A Safer Way To Play Tootsie Roll Industries

memoriesarecaptured/iStock Editorial via Getty Images

Shares of Tootsie Roll Industries, Inc. (TR) have fallen about 17.25% since I wrote my “taking profits in Tootsie Roll” article, but are up about 8.7% against a loss of 2.3% for the S&P 500 since I wrote my latest, cautious, piece on the company. This has me intrigued. This relative outperformance may indicate a greater appetite for Tootsie Roll’s unique taste than I had anticipated. The stock may have hit a bottom when I last looked at it. I want to determine whether it makes sense to buy at current levels, as the rest of the market seems to be going haywire. I’ll make that determination by looking at the updated financial history here, along with the stock as a thing distinct from the actual business.

I understand how painful it can be to read my stuff. For that reason, I’ll give you a statement of my thesis in this, the unimaginatively titled, “thesis statement” paragraph. I think this is a wonderful business. The cash flows are both predictable and steady, so I think the danger of a dividend cut is very low. My confidence in the business is boosted by the fact that the capital structure is very strong. The problem is with the stock. Tootsie Roll is too popular a bond substitute right now, and so the price is too rich for my blood. I think there’s a strong negative relationship between stock price and returns, and I think it would be best to continue to avoid the shares. Just because I’m not willing to buy at current prices doesn’t mean there’s nothing to do here, though. I’ve earned $4.70 selling puts on this stock over a very short period of time, and I intend to continue that profitable trend today. I write about the specific trade below.

Financial Snapshot

I’ve written before that I’m impressed by the capital structure here, and I’ve droned on in the past about how secure the dividend is at Tootsie Roll. If you want more detail about those aspects of the firm, I’d recommend reviewing my earlier work. For those who can’t stomach the prospects of that, I’ll just write that both cash flow per share and earnings per share have far outstripped dividends per share for some time. Additionally, unlike most other company’s I review, there are no significant contractual obligations that will take precedence over dividend payments, given the absence of any significant obligations. The following excerpt from the company’s latest 10-K expresses this as eloquently as any 10-K expresses anything.

Tootsie Roll (lack of) Contractual Obligations

Tootsie Roll 2020 10-K

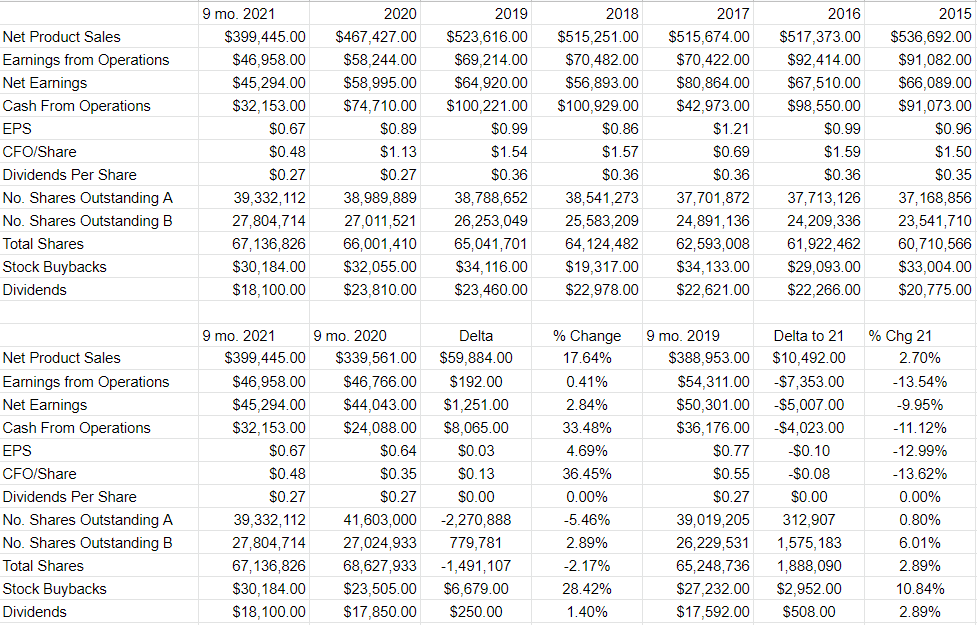

Finally, I previously complained about dilution. I considered it to be the only dark cloud in an otherwise sunny sky. It seems that the problem is being rectified as share count was down ~2% in the first nine months of 2021 relative to the same period in 2020.

In this missive, I want to zoom in on the most recent period, and compare it to previous periods.

The first nine months of 2021 saw revenue increase by ~17.6% relative to the same period in 2020, which is a startlingly good turnaround in my estimation. You may remember that 2020 was a unique year, though, and so I thought it’d be wise to compare 2021 to 2019. Revenue during the first nine months of 2021 was ~2.7% higher relative to the same period in 2019. Things get a bit less rosy when moving down the income statement. Net earnings was only ~2.8% greater in 2021 than it was in 2020, and was actually about 10% lower than it was in 2019.

This is because variable costs make up a relatively large component of total costs here. For instance, as revenue increased 17.6% in 2021 relative to 2020, total costs increased 20.4%. Selling and marketing expenses rose 20.6%, with the result that earnings from operations barely grew by .4%.

In summary, I don’t think there’s much worry about the dividend being cut here for the foreseeable future, but I don’t consider Tootsie Roll to be a growth machine. Investors shouldn’t expect growth from this business, any more than they should expect a cat to bark. That said, I’d be very happy to buy this bond substitute at the right price (i.e. with an embedded low growth assumption).

History of Tootsie Roll Finances

Tootsie Roll Investor Relations

The Stock

Welcome to the “Doyle becomes a downer” portion of the article. It’s at this point where I get into valuations, and it’s at this point where I frequently disqualify otherwise great companies from consideration as investments. I do this because I understand that a great company can be a terrible investment if it’s acquired at the wrong price. The fact is that a given company can be a great or terrible investment depending entirely on the price paid for it. I’ll drive this point home by using Tootsie Roll itself as an example. Someone who bought this on my birthday last year (December 2nd in case you forgot) is up about 5% since then. Someone who bought virtually identical shares only 2 weeks later is down just under 12% since then. This wild 17% swing in performance is entirely a function of the price paid for the stock, so we need to be mindful of the price paid. This is why I try to avoid overpaying for a stock, and insist on buying cheap.

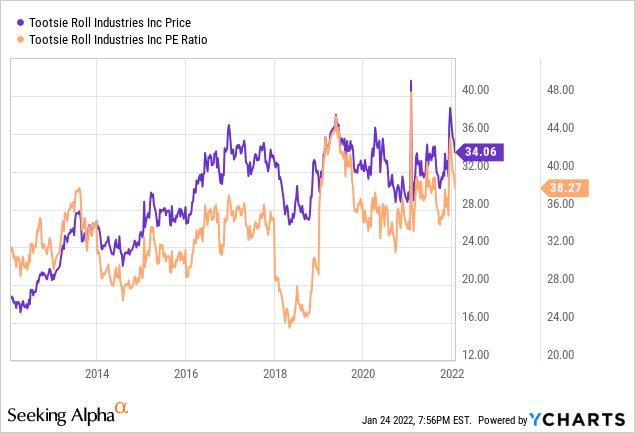

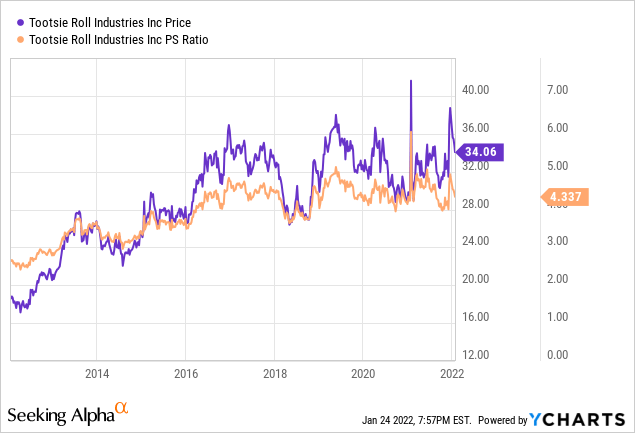

As you may recall, dear readers, I measure the cheapness (or not) of a stock in a few ways, ranging from the simple to the more complex. On the simple side, I look at the ratio of price to some measure of economic value like sales, earnings, free cash flow, and the like. Ideally, I want to see a stock trading at a discount to both its own history and the overall market. With that in mind, we see that the market is paying very near a decade high for $1 of future Tootsie Roll earnings, and sales, per the following.

In addition to simple ratios, I want to try to understand what the market is currently “assuming” about the future of this company. In order to do this, I turn to the work of Professor Stephen Penman and his great book that I can’t recommend highly enough “Accounting for Value.” In this book, Penman walks investors through how they can apply the magic of high school algebra to a standard finance formula in order to work out what the market is “thinking” about a given company’s future growth. This involves isolating the “g” (growth) variable in a fairly standard finance formula. Applying this approach to Tootsie Roll at the moment suggests the market is forecasting a growth rate of 10% for this business going forward, which I consider to be extraordinarily optimistic. Given all of the above, I can’t recommend buying this wonderful bond substitute at current levels. The dividend hasn’t increased since 2016. If management increased this, I’d reconsider, but for now I’ve got to take a pass on the shares.

Options Update

Just because I don’t want to buy at current prices doesn’t mean there’s no way to earn a profit here. As I pointed out in my earlier missive about Tootsie Roll, I’ve earned about $4.70 per share from selling put options on this name. In my estimation, that is rather extraordinary in light of the stock price, and the relatively short period of time I’ve been trading puts on this stock.

I like to try to repeat success when I can, so I’m going to write some more puts here. I’d be exceedingly happy to buy this stock at $25, so that’s the strike price I’m choosing. My regulars know that I consider short put options to be a “win-win” trade for a few reasons. Either the investor pockets a premium, which is never a hardship. If the shares trade below the strike price, the investor gets both the premium and the ability to buy a stock they like at an even more attractive price. This is also hardship-free in my view. Hence, “win-win.”

In terms of specifics, as I wrote above, I want a $25 strike price, because this corresponds to a 1.44% dividend yield. This isn’t a great yield, but in my view it’s not bad given the low level of risk present. So the specific put that I want to sell is the Tootsie Roll September put with a strike of $25. These are currently bid at $.55, which I consider a reasonable return for tying up capital for eight months. If the shares remain above $25 over the next eight months, I’ll simply add another $.55 per share to the $4.70 already earned here. If the shares fall, I’ll have an opportunity to buy this sustainable dividend at a net yield of ~1.44%. That’s also not a terrible risk adjusted return.

I hope everybody’s simultaneously “amped”, “pumped”, and “stoked” about the prospects of a “win-win”, because it’s that time again. That time where I pour sour milk all over the hopeful mood by writing about risk. The reality is that every investment comes with risk, and short puts are no exception. We do our best to navigate the world by exchanging one pair of risk-reward trade-offs for another. For example, holding cash presents the risk of erosion of purchasing power via inflation and the reward of preserving capital at times of extreme volatility. The risks of share ownership should be obvious to readers on this forum.

I think the risks of put options are very similar to those associated with a long stock position. If the shares drop in price, the stockholder loses money, and the short put writer may be obliged to buy the stock. Thus, both long stock and short put investors typically want to see higher stock prices.

Puts are distinct from stocks in that some put writers don’t want to actually buy the stock – they simply want to collect premia. Such investors care more about maximizing their income and will be less discriminating about which stock they sell puts on. These people don’t want to own the underlying security. I like my sleep far too much to play short puts in this way. I’m only willing to sell puts on companies I’m willing to buy at prices I’m willing to pay. For that reason, being exercised isn’t the hardship for me that it might be for many other put writers. My advice is that if you are considering this strategy yourself, you would be wise to only ever write puts on companies you’d be happy to own.

In my view, put writers take on risk, but they take on less risk (sometimes significantly less risk) than stock buyers in a critical way. Short put writers generate income simply for taking on the obligation to buy a business that they like at a price that they find attractive. This circumstance is objectively better than simply taking the prevailing market price. This is why I consider the risks of selling puts on a given day to be far lower than the risks associated with simply buying the stock on that day.

I’ll conclude this meandering discussion of risk by looking again at the specifics of the trade I’m recommending. If Tootsie Roll shares remain above $25.00 over the next eight months, the put seller will simply pocket a decent premium. If the shares fall in price, they’ll be obliged to buy at a price ~27% lower than the current level. Both outcomes are very acceptable in my view, so I consider this trade to be the definition of “risk-reducing.” I’m aware that writing about the risk-reducing potential of puts is a strange way to end a discussion of risk. Such is the world in which we live.

Conclusion

This remains a great business. The cash flows are very predictable, though I don’t expect much growth here anytime soon. The lack of growth isn’t a problem in my view in light of the rock solid capital structure. Companies vary quite a bit in terms of the sustainability and predictability of their cash flows. I like Tootsie Roll because it is sustainable, and it is relatively predictable. The problem, as is frequently the case, is the stock. It seems that I’m not the only one to have noticed the predictability of this thing, so the shares have bid up beyond what I consider to be reasonable. For that reason, I can’t recommend buying the shares. That said, I think the options market provides an interesting opportunity here. If you’re comfortable with put options, I’d recommend this or similar trade. If you’re not comfortable with puts, I’d recommend you make yourself comfortable with them, given their risk reducing, return enhancing potential. In the meantime, though, I’d wait until the share price falls to more closely align with value.

Published at Tue, 25 Jan 2022 17:24:13 -0800