Stock Market This Week – 05/13/23

Stock Market This Week

Stock Market This Week – 05/13/23

Inflation continues to moderate with another decent report. The Consumer Price Index (CPI) for April 2023 was down to 4.9%. The CPI peaked at 9.1% in June 2022, so progress is being made. However, the U.S. inflation rate is still above the 2% target. Similarly, the Producer Price Index is decelerating to 3.4% in April 2023 after peaking at 7.1% in March 2022.

But whether the U.S. Federal Reserve raises rates or not is open to debate. The Fed must balance inflation, employment, and now stress in the banking system. Fortunately, no more bank failures occurred in the past week.

Separately, oil prices continue to plummet, ending the week at about $70 per barrel. Weak demand in China and OPEC members’ inability to cut supply is causing prices to fall. In addition, the strong US dollar is helping. So if oil prices fall, gasoline costs per gallon should follow.

Whether a recession occurs is still a point for debate. With inflation falling and unemployment tied for a record low, a recession does not seem in the cards at the moment. However, failure to pass a new debt ceiling limit or slowing manufacturing may trigger a recession.

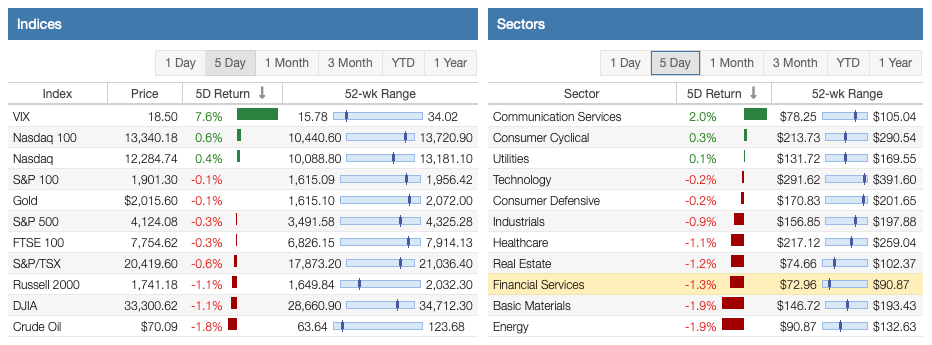

Stock Market Overview

The stock market had another mixed week.

As shown by data from Stock Rover*, the Nasdaq continues its dominance in 2023, led by mega-cap stocks, like Apple (AAPL), Microsoft (MSFT), and Meta Platforms (META). However, the S&P 500 Index, the Russell 2000, and the Dow Jones Industrial Average (DJIA) declined for the week.

Three of the 11 sectors had positive returns for the week. Consumer Services, Consumer Cyclical, and Utilities were the top three sectors for the week. But the Financial Services, Basic Materials, and Energy sectors performed worst.

Oil prices dropped by 1.8% to $70 per barrel, continuing its downward trend. The VIX rose and is still near its long-term average. Gold remained above $2,000 per ounce.

The Nasdaq is performing the best for the year, followed by the S&P 500 Index and the Dow 30, The Russell 2000 is down for the year. In addition, 7 of the 11 sectors are up year-to-date. The three best-performing sectors are Technology, Communication Services, and Consumer Cyclical. But the worst-performing sectors are Utilities, Financial Services, and Energy.

Affiliate

If you want to learn more about investing and dividends, then I suggest taking a course. The Simply Investing Course is a good value and fairly comprehensive. It consists of 10 modules and 27 lessons. You get lifetime access and 1-month access to the Simply Investing Report & Analysis Platform. Coupon Code – DIVPOWER15.

The Simply Investing Report & Analysis Platform analyzes 6,000+ stocks with 120 metrics and financial data. It include portfolios, watch lists, dividend income, e-mail alerts, etc. The best part is the list of top ranked stocks based on the 12 Rules of Simply Investing. Coupon Code – DIVPOWER15.

The dividend growth investing strategy has put in mixed returns as banks and energy stocks declined but is bouncing back. The table below shows their performance by category. Two of the four categories are in positive territory.

Affiliate

Portfolio Insight has 9,000+ stocks and ETFs in its database. You can get access up to dozens of metrics, 20-years of financial data from S&P Global, and our Dividend Quality Grade.

The Portfolio Insight platform gives users access to portfolio management, charting, screening and ranking, investment news, SEC fillings, stock analyses, etc. Try it free for 14-days.

Stock Market Valuation This Week

The S&P 500 Index trades at a price-to-earnings ratio of 23.87X, and the Schiller P/E Ratio is about 28.91X. These multiples are based on trailing twelve months (TTM) earnings.

The long-term means of these two ratios are approximately 16X and 17X, respectively.

The market is still overvalued despite the recent correction and a bear market and rebound. Earnings multiples of more than 30X are overvalued based on historical data.

Economic News This Week

Provided by Stock Rover*.

Energy Outlook

The U.S. Energy Information Administration (EIA), in its May 2023 Short-Term Energy Outlook (STEO), expects that U.S. crude oil production will rise by 640,000 barrels per day (bpd) to 12.53 million bpd in 2023 and by another 160,000 bpd to 12.69 million bpd in 2024. The EIA revised its forecasts for crude oil prices from its previous estimates, expecting the Brent spot price to average $79 per barrel in 2023, 7.5% lower than its April forecast. The 2024 forecast for the Brent spot price was also revised down – 8.3% to $74 per barrel in anticipation of an increase in global oil inventory.

The EIA projected U.S. gasoline prices to average $3.40 per gallon this summer, down from its April forecast of $3.50 per gallon. Rising refinery runs from global, and U.S. refiners anticipate the downward revision in U.S. gasoline prices. U.S. refinery runs are expected to reach their highest levels since 2019. In addition, the EIA forecasted the second most U.S. natural gas consumption for electricity generation on record for May thru September – averaging about 38 billion cubic feet per day (Bcf/d). Coal consumption in the electric power sector is expected to fall 13% in 2023 due to lower natural gas prices, more generation from renewable sources, and coal plant retirements.

Consumer Price Index

The U.S. Bureau of Labor Statistics reported the consumer price index increased (+0.4%) in April, after a (+0.1%) reading in March, (+0.4%) in February, and (+0.5%) in January. Over the last 12 months, the all items index is up (+4.9%) before seasonal adjustment as compared to (+5.0%) in March, (+6.0%) in February, and (+6.4%) in January. The index for shelter (+0.4%) was the most significant contributor to the monthly all-items increase, followed by increases in the index for used cars and trucks. (+4.4%) and the index for gasoline (+3.0%). The index for energy increased (+0.6%), with decreases in indexes for fuel oil (-4.5%), electricity (-0.7%), and natural gas (-4.9%), offsetting an increase in motor fuel (+2.8%).

Core CPI inflation which excludes food and energy, increased (+0.4%) in April, matching March’s reading, and follows (+0.5%) in February and (+0.4%) in January. The annual rate of core CPI inflation is now at (+5.5%), as compared to (+5.6%) in March, (+5.5%) in February, and (+5.6%) in January. The shelter index increased (+8.1%) year over year, accounting for over 60% of the total increase in Core CPI. Other indexes with significant gains over the last year include motor vehicle insurance (+15.5%), household furnishings and operations (+5.3%), recreation (+5.0%), and new vehicles (+5.4%).

Produce Price Index

The Labor Department reported that the Producer Price Index (PPI) for final demand increased by a seasonally adjusted (+0.2%) in April; this follows a (-0.4%) drop in March, (0.0%) in February, and (+0.4%) in January. The PPI is seen as a bellwether for inflation as it measures what suppliers charge businesses. The PPI index continued to decelerate to an annualized (+2.3%) in April; this follows (+2.7%), (+4.8%), and (+5.7%) reported for the prior three months. The high-water mark was set in March 2022 at (+11.7%). In April, 80% of the increase in the PPI is attributable to a (+0.3%) increase in prices for final demand services, which is the most significant increase since a (+0.4%) in November 2022. Over one-third of the rise in the index for final demand, services was due to a (+4.1%) increase in prices for portfolio management.

The index for final demand goods reported up (+0.2%), with a (+8.4%) increase in gasoline prices as a contributing factor. Conversely, the index for final demand foods decreased (-0.5%), as the index for chicken eggs dropped (-37.9%). Excluding food, energy, and trade services, the so-called core PPI increased (+0.2%) in April. The core PPI continued to decelerate to an annualized (+3.4%) in April, this follows (+3.7%), (+4.5%), and (+4.5%) readings for the prior three months. The high-water mark was set in March 2022 at (+7.1%).

Resources

Curated Weekend Reading From Around The Web

Portfolio Management and Investing

Retirement

Financial Independence

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Sure Dividend Pro Plan is an excellent resource for DIY dividend growth investors and retirees. Try it free for 7 days.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

- Portfolio Insight is the newest and most complete portfolio management tool with built-in stock screeners. Try it free for 14 days.

Receive a free e-book, “Become a Better Investor: 5 Fundamental Metrics to Know!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Prakash Kolli is the founder of the Dividend Power site. He is a self-taught investor, analyst, and writer on dividend growth stocks and financial independence. His writings can be found on Seeking Alpha, InvestorPlace, Business Insider, Nasdaq, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial sites. In addition, he is part of the Portfolio Insight and Sure Dividend teams. He was recently in the top 1.0% and 100 (73 out of over 13,450) financial bloggers, as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.

Published at Sat, 13 May 2023 07:06:49 -0700