As part of my monitoring process, I review the list of dividend increases. This process helps me review how the companies I own are doing. It also helps me identify companies for further research. I usually focus on the dividend increases for companies with a dividend streak longer than ten years in a row.

For this weekly review, I tend to focus my attention on companies with at least a ten year history of annual dividend increases, which also raised dividends last week. I provide a quick overview of each company that includes the amount of the most recent dividend increase, and compares it to its recent historical record. I also review the streak of annual dividend increases, and review earnings and valuation information.

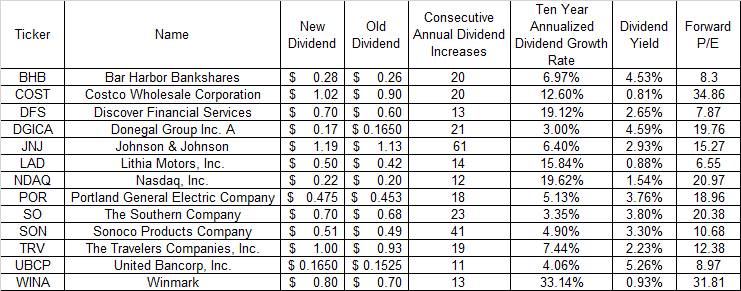

There were several notable dividend increases over the past week:

This list is not a recommendation to buy or sell stocks. It is simply a list of companies that raised dividends last week. The companies listed have managed to grow dividends for at least ten years in a row.

The next step in the process would be to review trends in earnings per share, in order to determine if the dividend growth is on strong ground. Rising earnings per share provide the fuel behind future dividend increases.

This should be followed by reviewing the trends in dividend payout ratios, in order to check the health of dividend payments. A rising payout ratio over time shows that future dividend growth may be in jeopardy. There is a natural limit to dividends increasing if earnings are stagnant or if dividends grow faster than earnings.

Obtaining an understanding behind the company’s business is helpful, in order to determine how defensible the dividend will be during the next recession. Certain companies are more immune to any downside, while others follow very closely the rise and fall in the economic cycle.

Of course, valuation is important, but it is more art than science. P/E ratios are not created equal. A stock with a P/E of 10 may turn out to be more expensive than a stock with a P/E of 30, if the latter is growing earnings and the former isn’t. Plus, the low P/E stock may be in a cyclical industry whose earnings will decline during the next recession, increasing the odds of a dividend cut. The high P/E company may be in an industry where earnings are somewhat recession resistant, which means that the likelihood of dividend cuts during the next recession is lower.