SPY: Rally May Just Be Getting Started As Inflation Narrative Collapses

epicurean/E+ via Getty Images

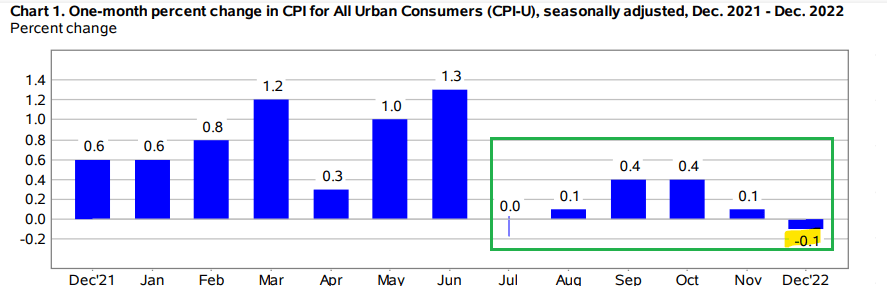

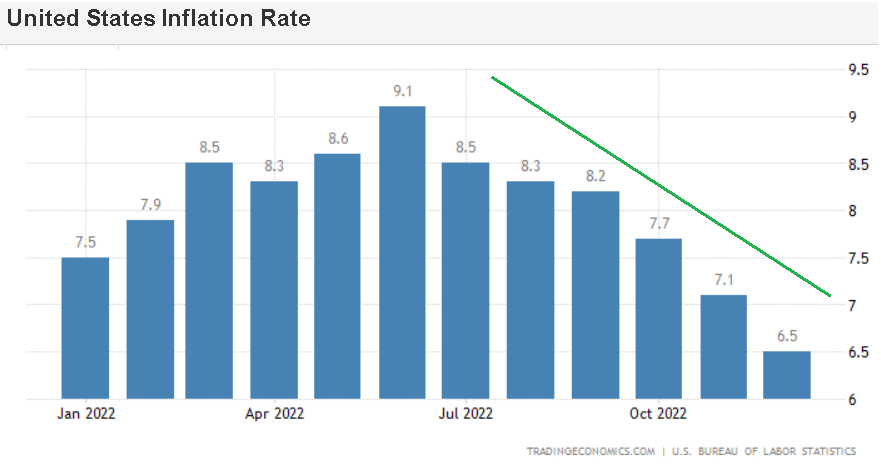

The December CPI came in at an annual rate of 6.5%, in line with the consensus, but also down from 7.1% in November. This was the lowest print since October 2021 echoing the trend in the “core” indicator at 5.7%, which excludes the impact of food and energy, also moving in the right direction.

More importantly, the monthly headline rate declined by -0.1%, surprising to the downside, compared to the flat estimate. If we consider the average monthly inflation over the last six months at just 0.15%, the pace implies an annualized forward rate for the CPI at just 2%.

source: BLS

The setup has significant implications for the next steps in Fed policy. An FOMC meeting is coming up in less than three weeks, with some new flexibility for Powell and company to start making adjustments to its uber-hawkish messaging that was the staple for much of 2022 because the data now justifies it.

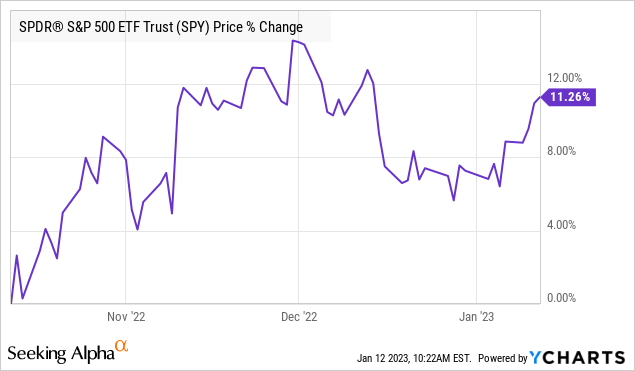

We’ve been calling it through several notes published here in recent months and on the right side of this trade considering the impressive rally already in stocks. The S&P 500 (NYSEARCA:SPY) is up nearly 15% from its October low and even compared to levels in May eight months ago. From here, we see several reasons to stay bullish and expect more upside.

Collapsing Inflationary Pressures

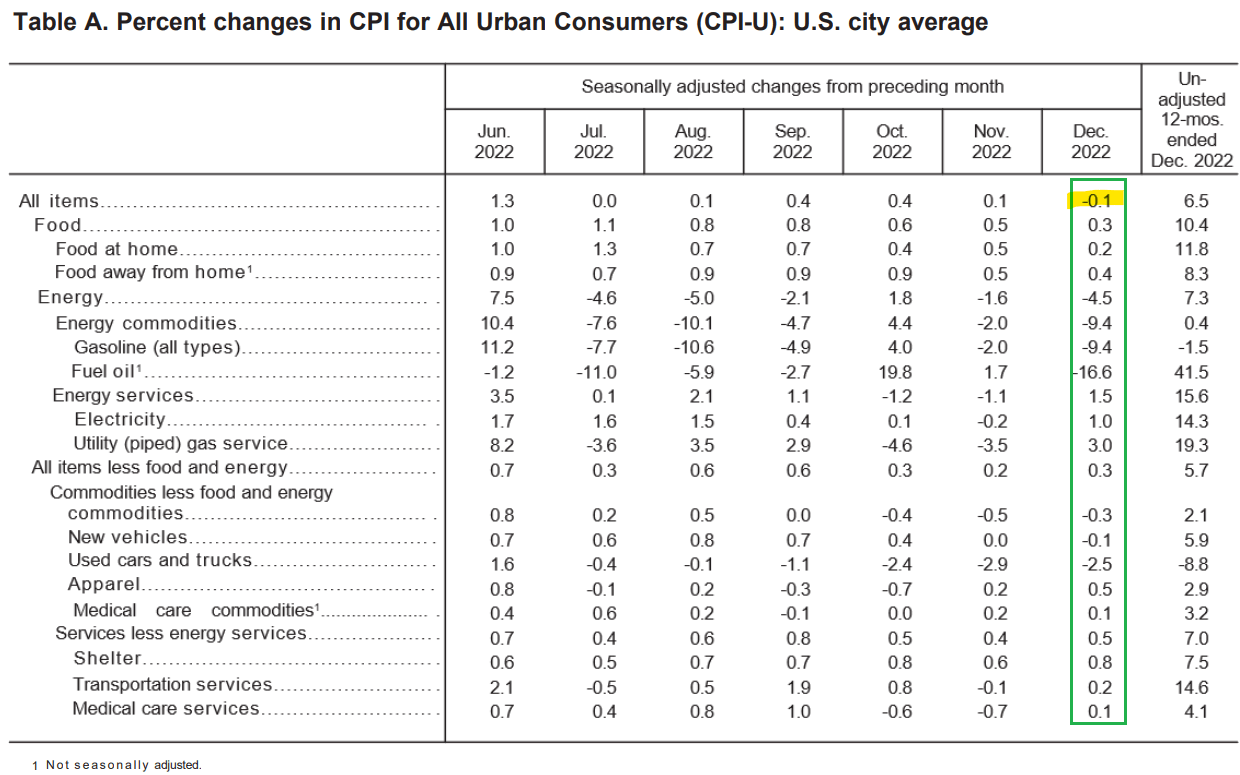

Going through the CPI data, a couple of points are worth diving into. The “food” price category posted a monthly increase of just +0.3%, the smallest increase since January 2021, nearly two years ago. The sense is that the combination of normalizing demand from skewed pandemic dynamics, easing supply chain pressures, and lower commodity input prices are starting to stabilize this high-profile category.

That’s also the setup in core items like “new vehicles”, and “used cards” where prices are dropping as inventory improves. The one stubborn component is “shelter” which still has room to fall, in our view, into the headlines of a slower housing market with the more direct impact of higher rates.

Lower energy prices are also helping based on broader global macro trends. On this point, most people will be aware of the sharp correction in oil and gas prices reflected in the “energy commodities” category declining by -4.5% on the month and up just 0.4% higher year-over-year. Beyond the daily volatility in crude oil (USO), what’s encouraging is the turn lower in “fuel oil” prices, down -17% m/m, which has been one of the hottest items over the past year. This implies the spread to oil is narrowing, again based on those same normalizing global supply chains.

source: BLS

The point here is to say that there are plenty of indications inflation as we saw it in 2022 is effectively over. Entering 2023 with the January and February data, the CPI will start hitting tough comps from the first half of 2022. A headline inflation rate under 3% by the end of this year could be in the cards as a very bullish turn of events.

source: tradingeconomics

Bullish On Stocks

As it relates to the Fed, it’s not “mission accomplished” just yet, but it’s clear to us that the data has progressed better than expected, and it may not be necessary for many more rate hikes.

One of our talking points has been that the Fed played it extra cautiously, in the face of damaged credibility following its missteps in 2021. In other words, they may have underpromised last year through the fire and brimstone messaging to make room to eventually over-deliver. That’s the trajectory we believe is taking place.

Whether the next Fed Meeting set for February 1st features a 50 basis point hike, or now the more likely a 25 basis point increase; we’re one step closer to reaching that terminal rate. Into the second half of the year, a scenario where it’s evident forward inflation expectations are firmly anchored in the low single digits can place a decision for a possible rate cut on the table.

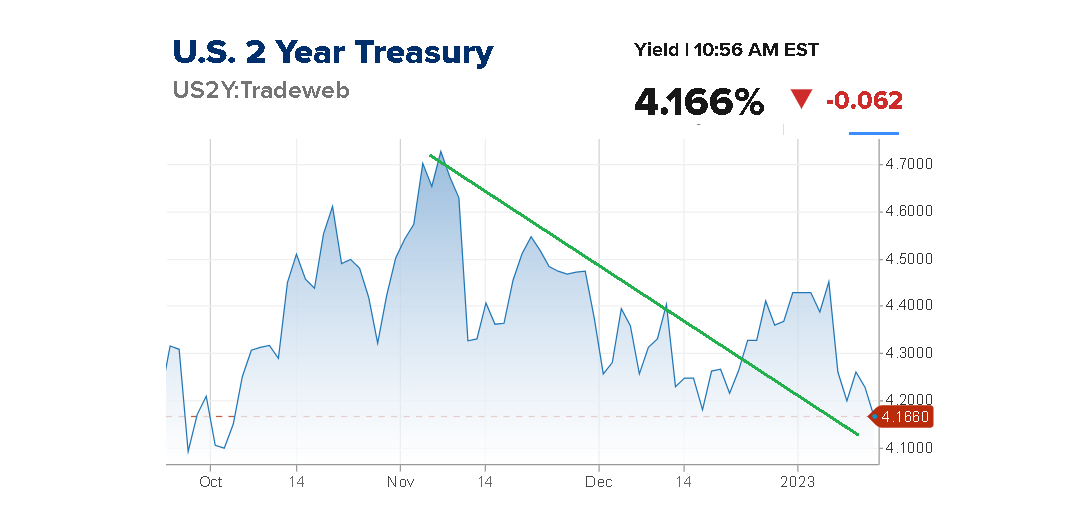

This of course would work to jumpstart investment sentiment with a boost to economic activity as a strong tailwind for risk assets. We’re already seeing that with the action in Treasuries as yields pull back with a rally in bonds in recent months. This is the market’s inference for where Fed policy is headed going forward.

source: cnbc

The biggest change today is that the latest data sort of forces a reckoning by investors in the large segment of the market that came into 2023 with a baseline of “higher for longer” in terms of interest rates, or even those that thought that inflation was poised to re-accelerate higher. This also ties into the otherwise resilient labor market data which has posted continued job gains even as wage pressures slow.

Any calls for surging unemployment and a deeper economic collapse are moving more toward the side of dangerously contrarian. At the end of the day, the Fed may achieve its goal of stabilizing consumer prices without causing a deep recession which is a nugget many believed to be impossible.

What we’re counting on is a clearer path for a “soft landing” in the U.S. economy where despite the volatile conditions last year, the economy emerges relatively unscathed, where the higher plateau for interest rates is manageable. The next stage in the cycle could be marked by good-news is good-news with several soft and hard indicators suggesting a broader macro rebound. A lot of that will be tied directly to the easing inflation.

- Corporate margins and earnings benefit from lower cost pressures.

- Consumer sentiment gets a lift.

- Manufacturing and Services PMI bounce from near record lows.

- Stabilizing interest rates provide a floor to the housing market.

- China reopening leads to a rebound in trade activity.

- Further improvements to supply chains.

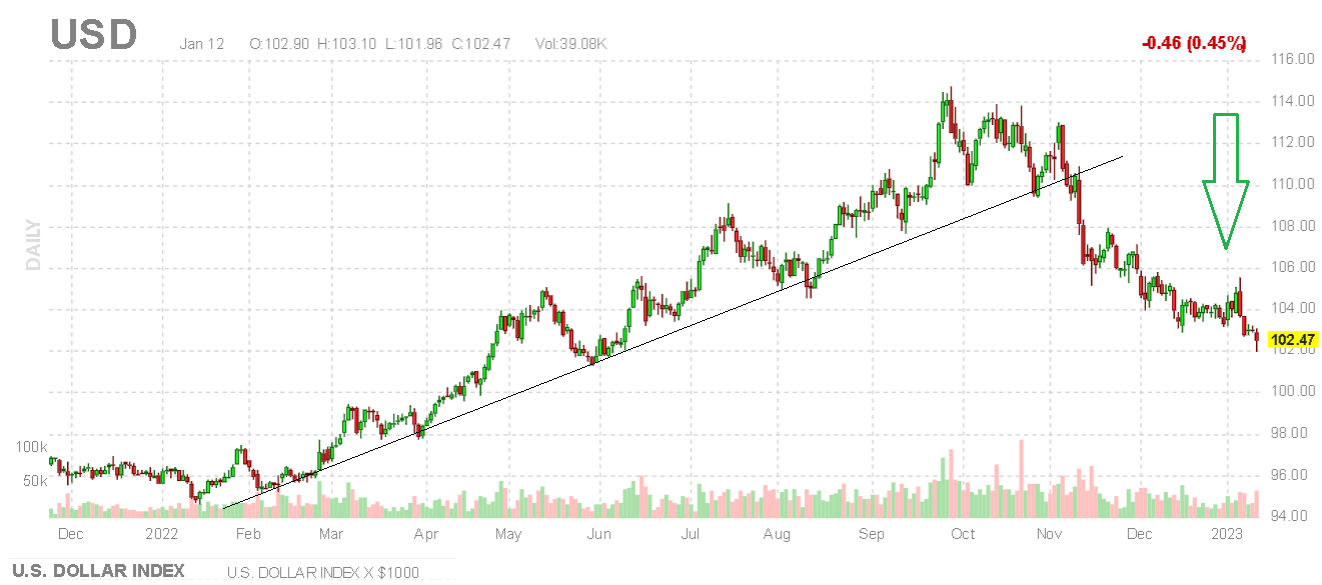

Maybe the biggest development in recent months has been the weakening of the U.S. Dollar corresponding to the pullback in bond yields, along with the specific trends towards the Euro as the large component of the Dollar Index. The message we have is that while higher interest rates represent a form of monetary tightening, the weaker Dollar and now lower inflation expectation help to balance those impacts. A resurgence of global growth including momentum in emerging markets also ends up being positive for the macro backdrop.

source: finviz

Q4 Earnings Season Preview

The next major market catalyst will be the upcoming Q4 earnings season which kicks off with the big banks reporting Friday, January 13th while most mega-cap leaders come later this month.

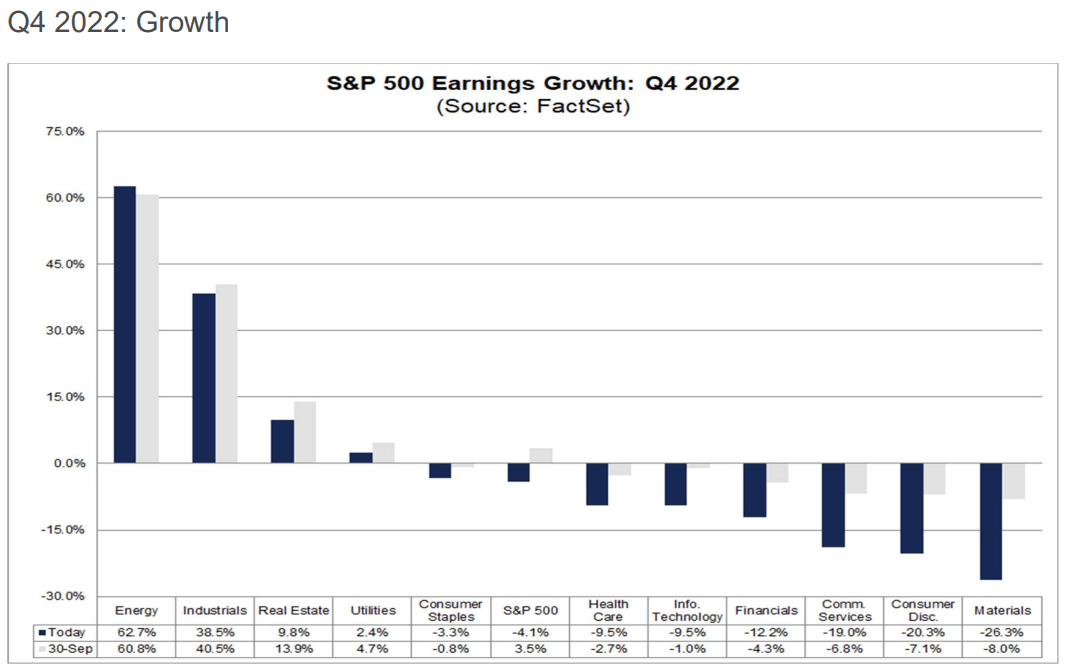

The data we’re looking at suggests earnings estimates have trended lower in recent months which is in the context of what until a few weeks ago was extreme pessimism and now a low base of expectations. According to FactSet, the S&P 500 EPS is on track to post an annual decline of -4.1%. This is against the historically strong Q4 2021, with weakness, particularly from consumer discretionary names and also tech.

source: FactSet

At the same time, consider that the sectors facing the biggest earnings headwinds have also lagged with a case to be made that their poor performance suggests that some of the earnings weakness has already been priced in.

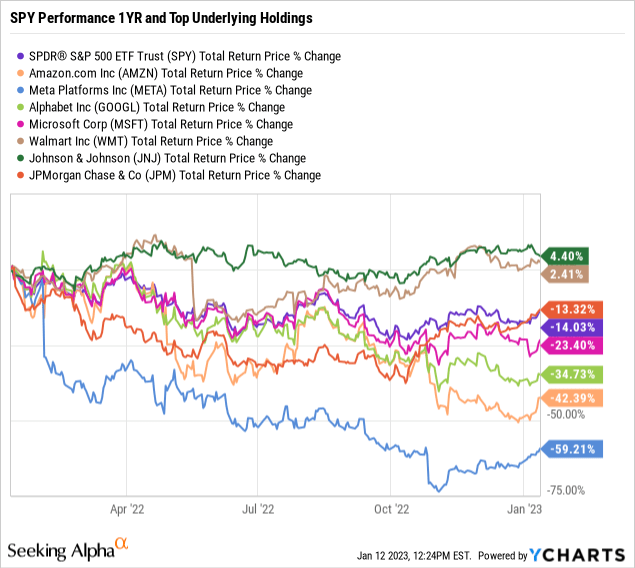

Major companies like Amazon.com (AMZN) previously cited inflation and logistics costs as one of its biggest challenges last year, which is encouraging considering those factors are reversing now. We’ve called AMZN a big winner from the November CPI report and the latest December data further supports that view.

There is also a thought that efforts toward cost-cutting and driving financial efficiencies can play a bigger role going forward. That’s the case with Meta Platforms, Inc. (META), among the worst performers in the S&P 500 but notably gaining momentum with a rally.

With banks the big question is, how have the higher interest rates impacted core lending beyond the positive income factor? One trend that will be watched is how large of loan-loss provisions the group including JPMorgan Chase & Co. (JPM) chooses to take as a sign of financial concerns. On that point, we haven’t seen the widescale corporate defaults defined in other recessions which is a good sign for earnings momentum from financials.

Overall, it will be important for companies to confirm conditions have remained at least stable relative to Q3 when 40% of S&P 500 companies were able to beat EPS expectations. A cautiously optimistic outlook from management teams focusing on improving supply chains along with easing cost pressures as a positive for margins can go a long way for the market to climb the wall of earnings worry.

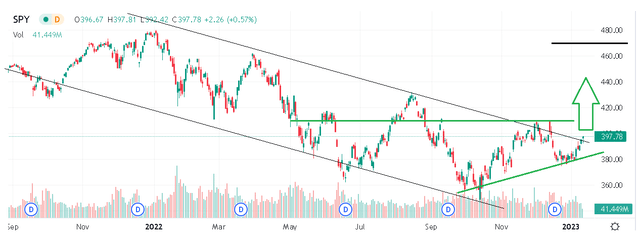

SPY Price Forecast

The way we see it playing out is that beyond Q4 earnings reports from major companies, the February FOMC meeting incorporating the latest CPI data could be a game changer through a new narrative in the market consensus. An environment where bears begin to slowly abandon calls for the market to make a new cycle low translates directly into a short squeeze at the margin as a tailwind for stocks to run.

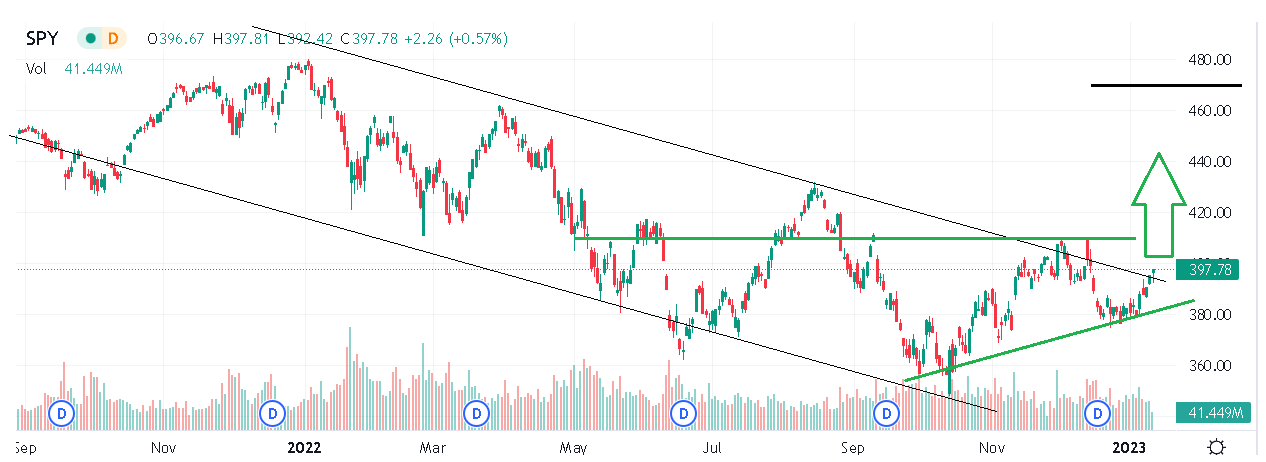

A bullish positioning into this positive market momentum makes sense. We’ve previously set a year-end price target for the S&P at 4,777 or nearly $480 in SPY and reaffirm that call today. SPY is approaching the $400 or $4,000 at the S&P 500 index level which is a key psychological level. Beaten-down names, particularly in tech and growth, are well-positioned to lead higher.

In terms of risks, we always have to bring up the ongoing Russia-Ukraine conflict which remains volatile. All it takes is a headline of some escalation into NATO territory where all bets are off. We’ll consider this more of a tail-risk event but needs to be watched closely. Energy prices are also critical going forward. Even with some room for oil to rebound from here, as the sharply higher price of gasoline and fuel could drive a new wave of inflation.

Seeking Alpha

Published at Thu, 12 Jan 2023 12:57:18 -0800