Roth IRA’s for Dividend Investors

Nothing is certain in this world except for death and taxes. For many dividend growth investors, this could be characterized as a feeling that they are being taxed to death. I am always on the lookout to legally minimize my investment taxes as much as possible. In fact there is an easy way to invest in dividend paying stocks without ever having to pay taxes on your investment.

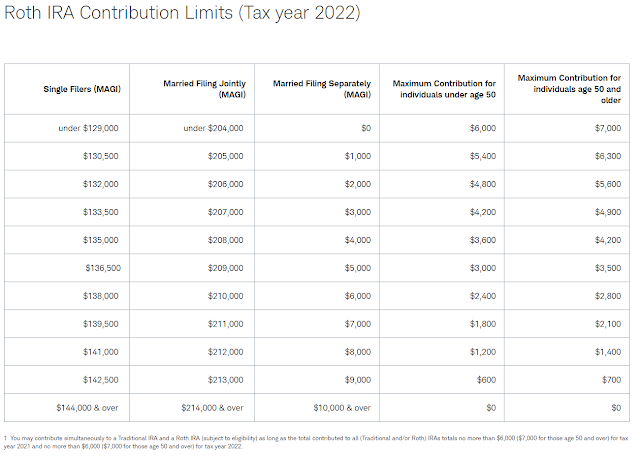

The Roth IRA allows individuals who have earned income in a given year to contribute up to $6000 in after-tax dollars to their retirement account. There is a catch-up contribution of $1000 for individuals who are 50 years of age or older. While contributions to Roth IRA’s are not deductible on your tax returns, earnings and principal distributions are tax free once certain age and time requirements are met.

The earned income includes compensation from salary, wages, commissions, bonuses and alimony. Income from interest, dividends, annuities or pensions does not count as earned income in the eyes of the IRS.

The contribution limit for a Roth IRA is the same as the contribution limit for a regular IRA. However the amount that can be contributed to a Roth IRA is the amount remaining after subtracting any contribution made to a regular IRA. This means that if you contributed the maximum allowable amount to your regular IRA of $6000, you would not be able to contribute anything to a Roth IRA in that year.

Source: Schwab

In order to avoid paying taxes on distributions from Roth IRA accounts, investors need to become acquainted with the qualified nontaxable distribution rules.

According to the IRS, qualified nontaxable distributions for Roth IRA’s are those made at least 5 years after the taxpayer’s first contribution to a Roth IRA and made:

2) To a beneficiary after the death of the taxpayer

3) Because the taxpayer becomes disabled

4) For a use of a first time homebuyer

The biggest benefits of a Roth IRA are the long-term tax free compounding of capital, the fact that qualified distributions are tax-free and the fact that there are no required minimum distributions. Another little known fact behind Roth IRA’s is that direct contributions may be withdrawn at any time. This makes them a perfect investment vehicle for investors who plan on retiring early and living off dividends before they reach typical retirement ages of 60 years.

I hold a portion of my assets in a Roth IRA. While the contribution limit is only $6,000, that is still a good start. For a married couple maxing out their Roth IRA’s, you have $12,000 to invest.

– Kinder Morgan Partners – One Company three ways to invest

– Philip Morris International (PM) Dividend Stock Analysis

Published at Wed, 17 Aug 2022 09:00:00 -0700