MasterCraft: Significantly Undervalued With Secular Growth Prospects

JulPo/E+ via Getty Images

Are you interested in consumer cyclical and industrial stocks while being worried about the macroeconomic outlook? Well, if you are, then MasterCraft (NASDAQ:MCFT) should be on your watchlist.

Today’s analysis discusses MasterCraft’s Veblen good status and how the company could resume its robust growth trajectory during trying economic times. In addition, the stock is valued on an absolute and relative basis, providing a valuable quantitative overlay.

I hope you enjoy the article, and I look forward to debating matters in the comments section!

Veblen Good Status

A Veblen good is a type of product that serves high-income individuals. Thus, companies like MasterCraft that retail Veblen goods are generally less susceptible to downside income elasticity.

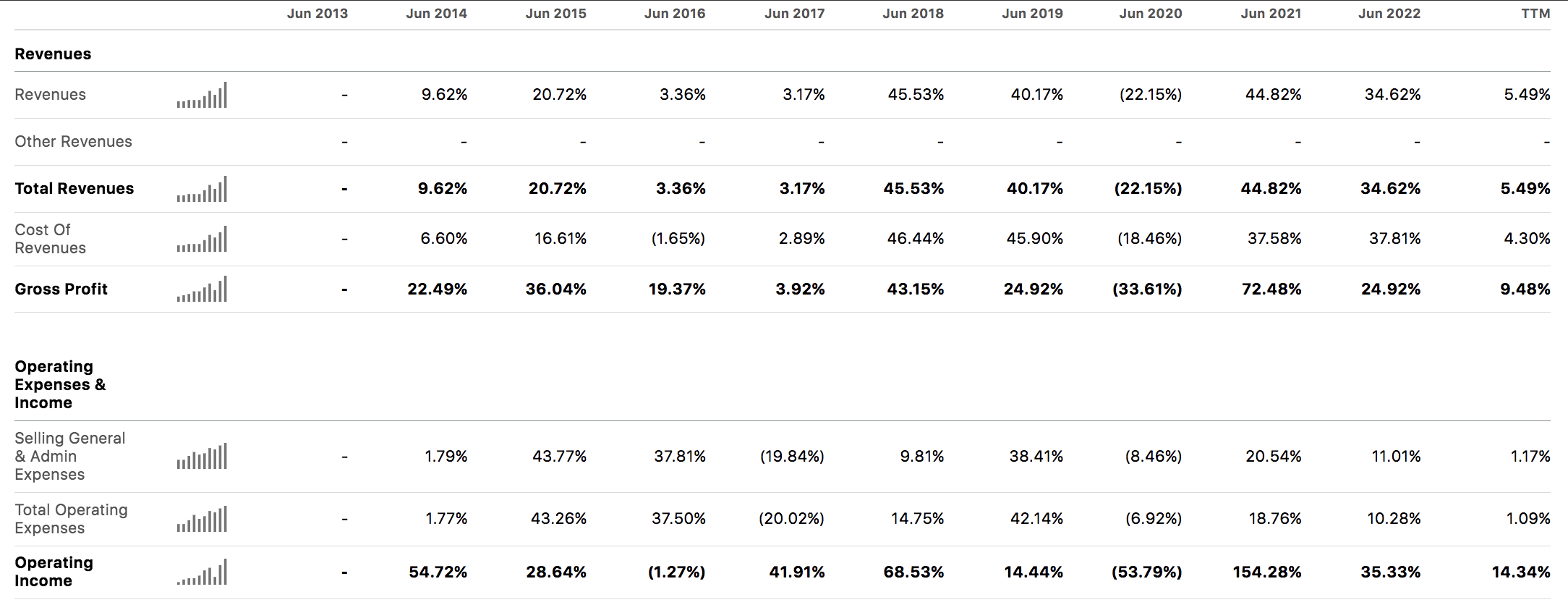

Mastercraft’s consistent historical operating income growth corroborates its Veblen status argument as it’s been able to stroll through economic downturns apart from 2020 when it was restricted by covid lockdowns.

MasterCraft Income Statement Growth Rates (Seeking Alpha)

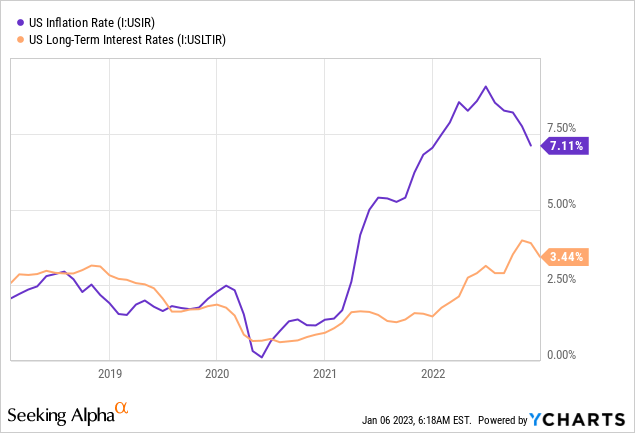

Economic staleness is anticipated during 2023 as inflation remains resilient and economic growth rates are waning. Moreover, central banks probably won’t be able to stimulate economic growth until inflation settles within its acceptable bounds of 2% to 3%.

However, Veblen goods could provide a hedge against a potential economic blip. MasterCraft’s luxury high-end boats cater to a small portion of the population, which seemingly isn’t as affected by adverse economic cycles.

Operational Review

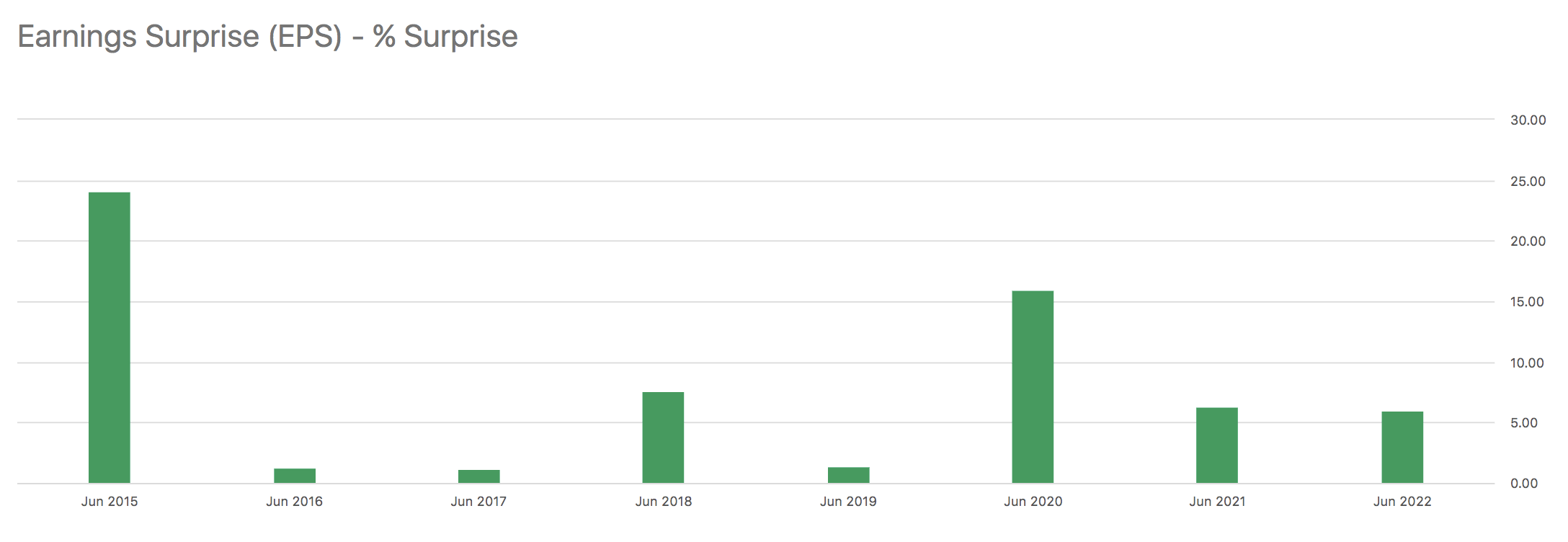

During its latest fiscal quarter, MasterCraft made a strong showing, beating revenue estimates by $4.26 million at a year-over-year growth rate of 29.8%. Moreover, the company dominated its earnings-per-share expectations by 14 cents.

MasterCraft has a history of beating its earnings-per-share targets. Beating earnings-per-share is often interpreted as “earnings momentum” by investors, which could, in turn, lead to stock price momentum. Therefore, I think this feature could result in valuable anomalies.

Seeking Alpha

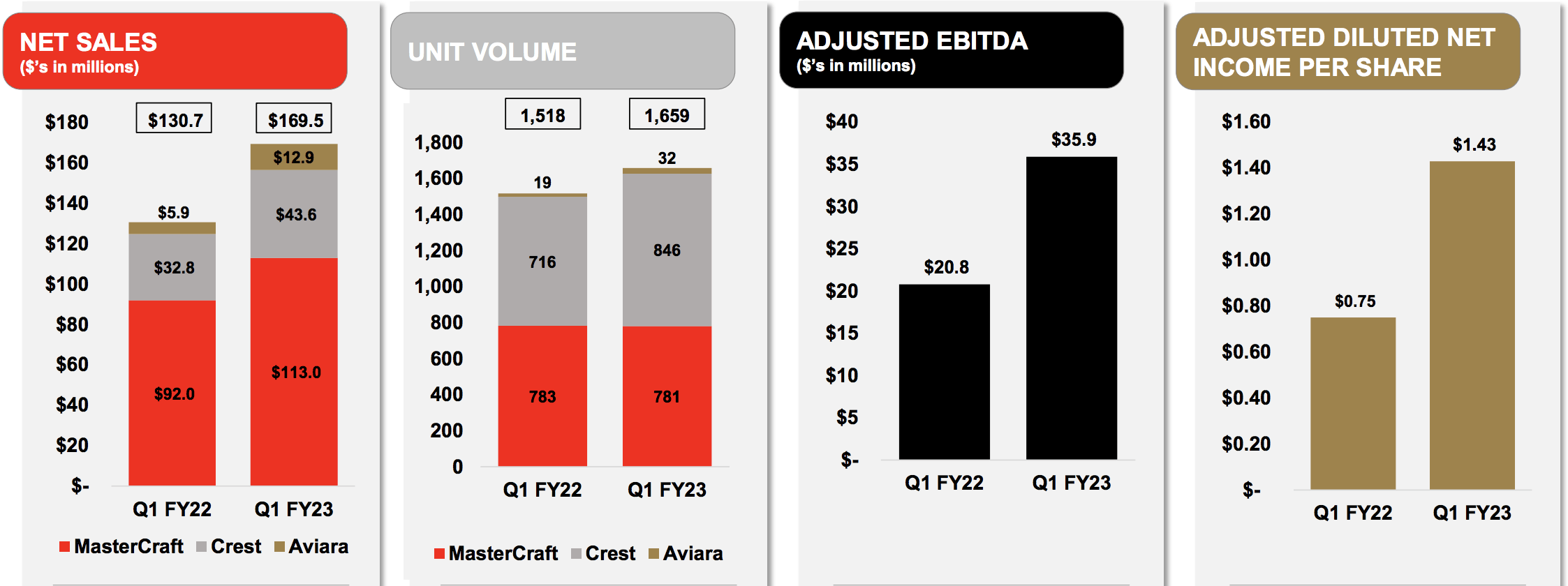

The firm delivered significant growth across the board in its latest quarter, with its unit volumes increased by 9.3% year-over-year. In addition, MasterCraft’s Adjusted-EBITDA and net sales surged by 72.8% and 29.7%, respectively.

MasterCraft

The company has experienced tremendous success from its wholesale unit, delivering year-over-year growth of 9.3%. MasterCraft’s Aviara brand has reached profitability, while Crest has continued its momentum by posting record gross profit margins. Although the firm is luxury-centric, its portfolio hosts a range of product offerings, allowing cross-market sales synergies.

MasterCraft

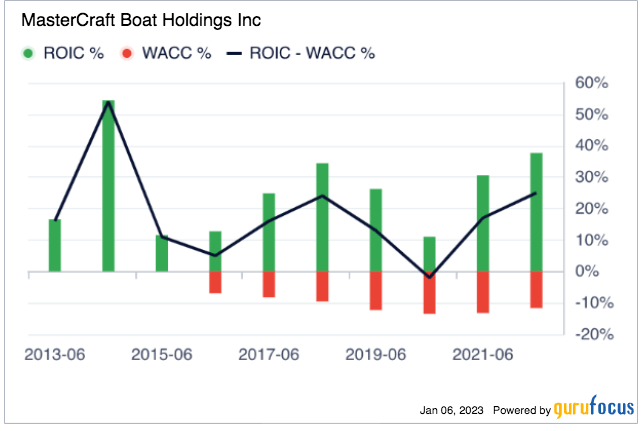

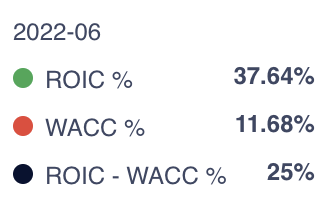

Furthermore, MasterCraft’s return on invested capital is robust, exceeding its weighted average cost of capital by a significant amount. The ROIC metric measures how well a company deploys its capital and is often an indicator of a stock’s residual value.

Gurufocus

Gurufocus

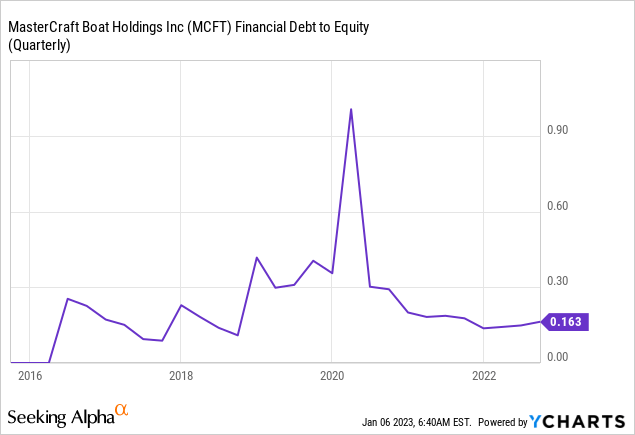

Lastly, an abundance of shareholder value is being passed down as the company operates with a moderate debt-to-equity ratio. Increased leverage could proliferate sales; however, low leverage is desirable during worrisome economic climates as it compresses a firm’s earnings volatility.

An Undervalued Security

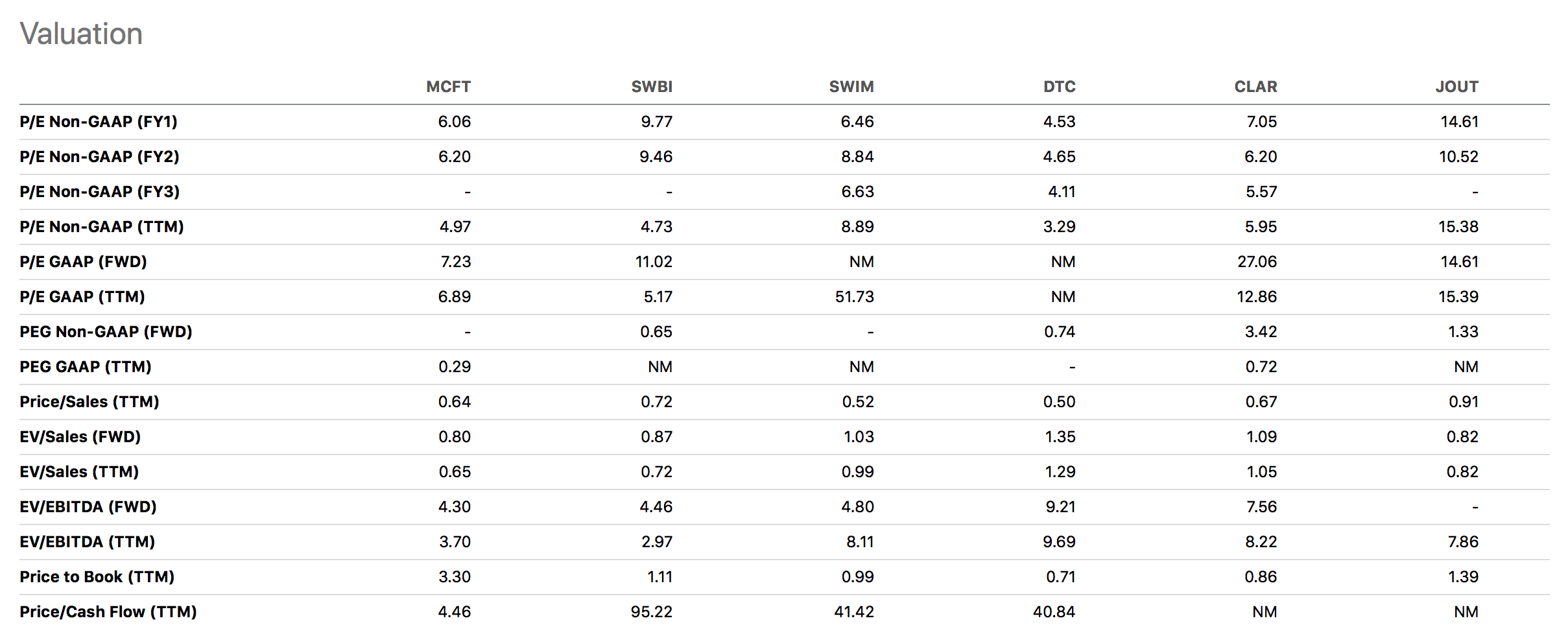

At face value, MasterCraft is incredibly undervalued, with its stock trading at a price-to-sales discount of approximately 1.56x. Additionally, the stock’s price-to-earnings and EV/EBITDA multiples are at cyclical discounts worth approximately 46.32% and 51.54% each.

A peer analysis suggests that MasterCraft is undervalued compared to comparable stocks. Because the company is asset-heavy, its price-to-book speaks volumes. Thus, its price-to-book of 3.3x should be considered a critical risk, which investors must keep tabs on.

Peer Analysis (Seeking Alpha)

“Top of my head” math suggests that $40.33 presents a fair value for MasterCraft, and a 10% downside margin of safety still places the asset’s intrinsic value above its current market price (around the $26 handle).

My rough sum consists of multiplying the stock’s 5-year average PE ratio (to account for cyclicality) with analysts’ estimated year-end EPS ratio. The formula I utilized is known as the “PE expansion formula ” and provides a valuable indicator but should never be considered in isolation.

Notable Risks

Regardless of its Veblen status, we’re still looking at a cyclical stock here, meaning it is more sensitive to the economic cycle than risk-off assets such as consumer staple stocks, sovereign bonds, and cash. Thus, a continued market drawdown could eventually drag MasterCraft into the abyss.

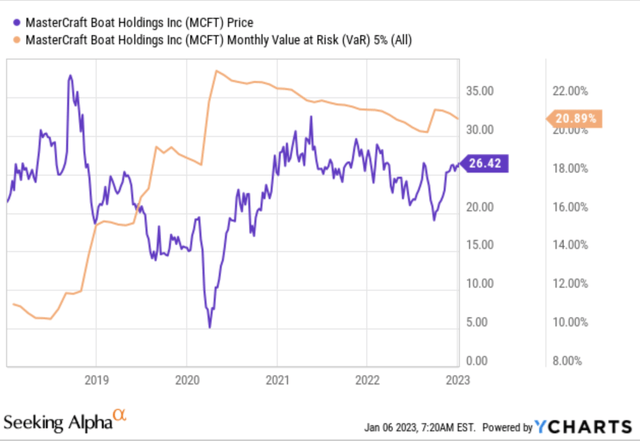

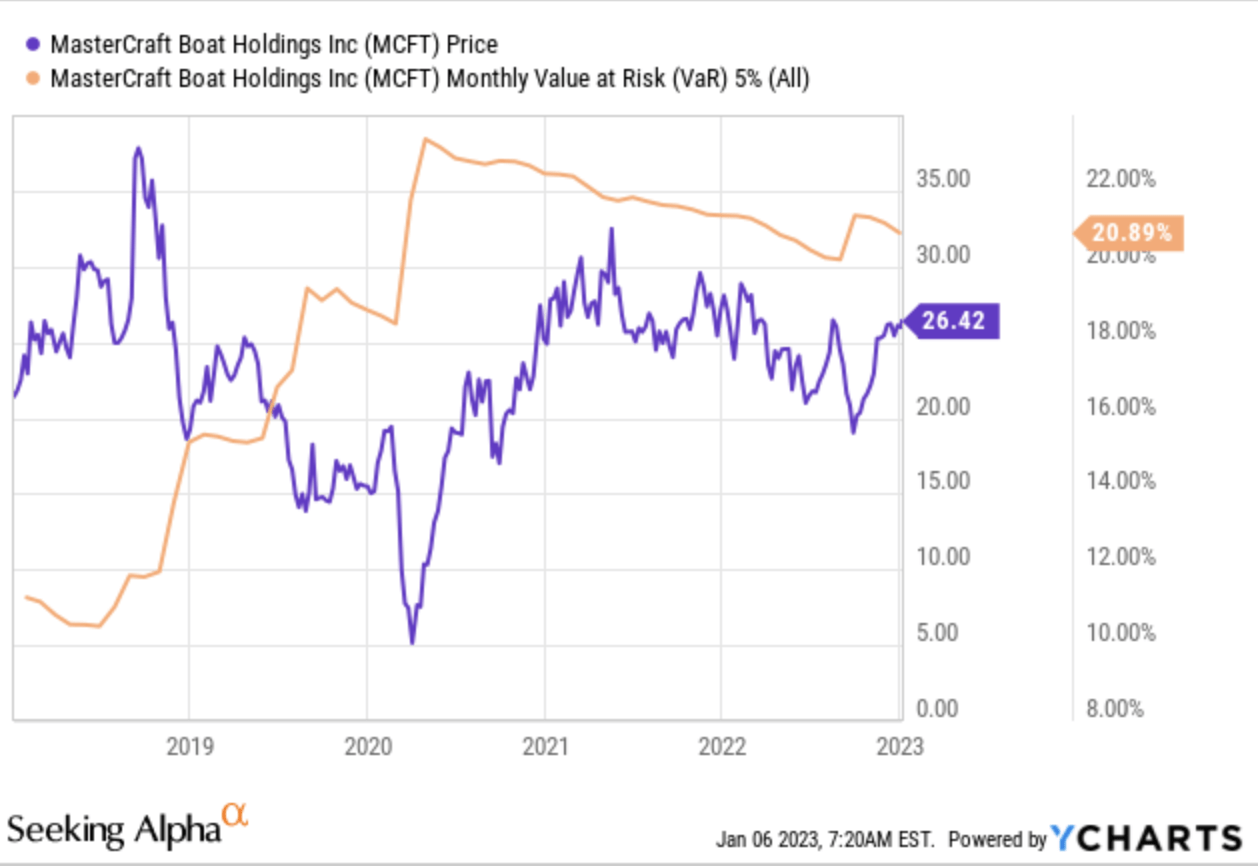

Furthermore, the stock possesses an unfavorable value-at-risk number. MasterCraft’s monthly Var (5%) suggests the stock will likely lose at least 20.89% in 5% of its traded months. Thus, it’s unnecessary to say that this security will add additional risk to your portfolio.

Seeking Alpha; YCharts

Final Word

I’m a consumer cyclical contrarian at this stage, stemming from my skepticism of today’s economy. However, MasterCraft could be an outlier this year as its Veblen status phases out downside income elasticity risk. Furthermore, the company possesses solid cross-market sales opportunities and hosts little debt.

At face value, MasterCraft’s stock is undervalued relative to its peers and on an absolute basis. Thus, I/we assign a strong buy rating with a 12-month horizon.

Published at Fri, 06 Jan 2023 13:15:22 -0800