ChargePoint: Buy This EV Charging Stock Ahead Of Upcoming Earnings

robertcicchetti/iStock Editorial via Getty Images

ChargePoint (CHPT) is the largest EV charging station company in North America with over 163,000 ports spread out across the United States, Canada, and Europe.

I’ve been extremely bullish on this company since ChargePoint completed its SPAC merger despite a rocky selloff in the EV sector. To put it bluntly, EV stocks got crushed in November 2021 when billionaires such as Elon Musk began dumping their tech stocks holdings.

TSLA), Lucid (NASDAQ:LCID), Rivian (NASDAQ:RIVN), Ford (NYSE:F), etc. However, I’m buying up shares of CHPT as a “pick and axes” play on the growing EV sector.

TSLA), Lucid (NASDAQ:LCID), Rivian (NASDAQ:RIVN), Ford (NYSE:F), etc. However, I’m buying up shares of CHPT as a “pick and axes” play on the growing EV sector.

Nearly 6.5 million EVs were sold worldwide in 2021 and I expect that number to increase dramatically due to enhanced consumer awareness of renewable energy vehicles and word of mouth.

Here are a few examples of explosive YoY growth:

| Company | Total 2021 EVs Delivered | YoY Growth |

| Tesla | 936,000 | 87% |

| Nio | 91,429 | 100% |

| Xpeng | 98,155 | 263% |

| Ford | 27,140 | N/A |

Source: Author, with data from Seeking Alpha

The crazy part is that this is just the beginning of a massive explosion in EV adoption. Legacy car makers such as GM (NYSE:GM) and Toyota (NYSE:TM) are working day and night to catch up to the competition. Canoo (NASDAQ:GOEV), Lordstown Motors (NASDAQ:RIDE), and Polestar (NASDAQ:GGPI) will scale their production numbers this year and you’re going to see a lot more EV sightings out on the road.

ChargePoint is a Pure “Picks and Shovels” Play on Exponential EV Adoption

ChargePoint is a software company that generates revenue from physical hardware sales and ongoing subscription revenue. The company uses an asset-light business model to scale its revenue without incurring huge capital costs.

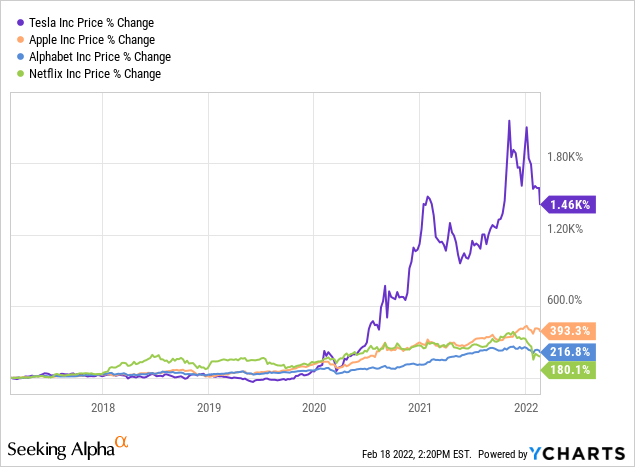

The most dominant company in any fast-growing industry tends to outperform the rest of the pack and produce superior returns for shareholders. Think about companies like:

- Tesla: Leader of the EV Industry

- Apple (NASDAQ:AAPL): Leader of the Tech Industry

- Alphabet (NASDAQ:GOOG): Leader of Online Search

- Netflix (NASDAQ:NFLX): Leader of paid online video streaming

Just take a look at the returns of the aforementioned companies over the last 5 years and see for yourself.

YCharts

YChartsThis is the same reason why I’m so excited about ChargePoint. They have the opportunity to achieve similar returns within a new industry that’s set to explode.

ChargePoint Leads All Other EV Charging Companies in Total Revenue

ChargePoint isn’t the only company going after the EV charging market and even Tesla opened its supercharging network to all EVs last year.

There are some tough competitors but ChargePoint leads the market by a longshot.

| Company | TTM Revenue |

| ChargePoint (NASDAQ:CHPT) | $204 million |

| EVgo (NASDAQ:EVGO) | $19 million |

| Volta (NYSE:VLTA) | $28 million |

| Blink Charging (NASDAQ:BLNK) | $15 million |

Source: Author, with data from Seeking Alpha

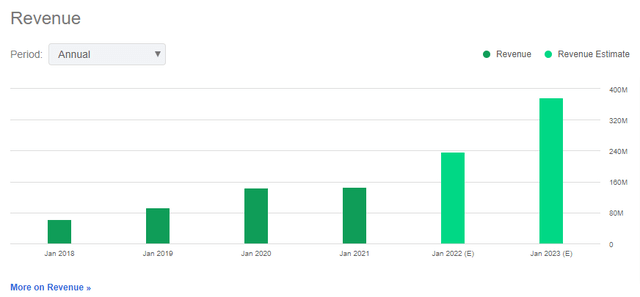

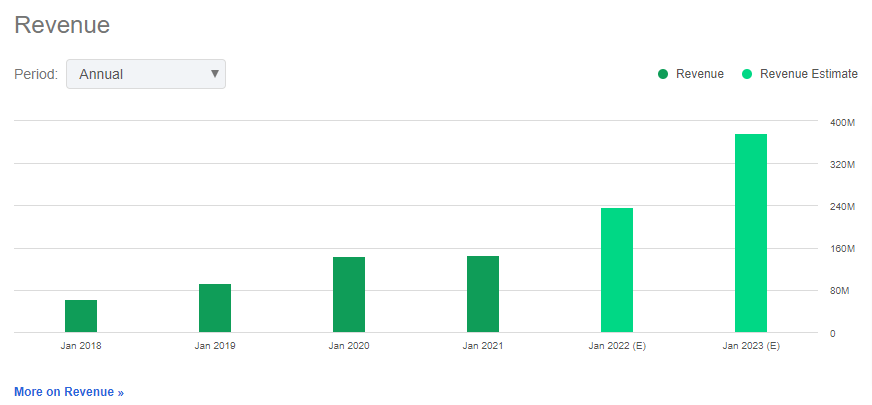

ChargePoint is expected to reach $378 million in revenue by 2023, which means CHPT stock is currently valued at a future Price to Sales ratio of 12.

SeekingAlpha.com

SeekingAlpha.com

Risk Factors

ChargePoint has a plethora of competitors who all want a piece of the EV industry. Tesla’s supercharging network is the biggest competitor in America while other competitors such as Blink Charging and EVgo are showing promise.

Many ChargePoint bears argue that the majority of ChargePoint’s stations are level 2 chargers instead of fast level 3 chargers.

It’s true that many consumers will charge on the go but most EV owners charge their vehicles at home overnight or during their work shift. ChargePoint does support level 3 chargers and has made recent acquisitions to grow its revenue in Europe.

If level 3 charging makes up the bulk of the industry revenue years ahead then ChargePoint will need to invest lots of capital to update its network. However, revenue continues to grow and I think the company is moving in the right direction.

Another potential risk factor is the rise of solar powered cars. New startups plan to produce vehicles that charge using solar power without needing a charging station.

Aptera will begin selling a 400-mile range solar-powered vehicle this year with prices starting at $29,800.

The good news is that EV battery technology costs are dropping every year and many consumers are satisfied with the current EV charging options.

Conclusion

I look for high-growth companies with leading market shares in fast-growing industries when conducting my research for articles on Seeking Alpha. ChargePoint checks off all the boxes when it comes to solid management, revenue growth, market share, asset-light business model, and future revenue growth opportunities.

It may take a few years for ChargePoint to reach profitability but I believe it’s worth the wait. CHPT shares trade near the $10 range and Q4 2021 will reveal a lot about the company’s guidance in 2022.

EV sales soared in 2021 and that means ChargePoint should have a stellar Q4 2021 earnings report as well. I’m really bullish on this company and am looking forward to watching it grow.

Published at Fri, 18 Feb 2022 16:33:40 -0800