Blackrock (BLK) Dividend Stock Analysis

Blackrock (BLK) is the largest investment manager in the world, with over $6.5 trillion in assets under management.

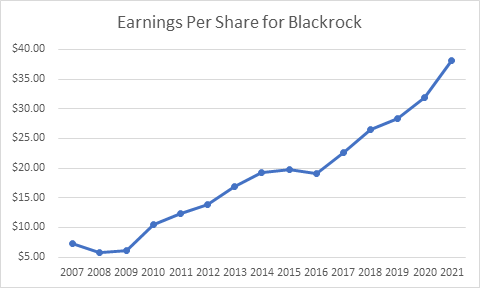

Over the past decade, the stock has compounded by 19.57%/year. Future returns will likely be lower, and they will track growth in earnings per share and the initial dividend yield at the time of investment.

The company is a leader in the asset management industry, with tremendous scale. It also has a diversity of products offered (equity, fixed income etc), geographic diversity ( Americas, Europe, Asia etc) in its products offered and the types of strategies offered ( active, passive, cash management). The company also has diversity in clients served – retail & institutional.

The company is a leader in ETFs, with tremendous inflows coming its way as there is a trend to switch from high cost mutual funds to ETFs. Unfortunately, passively managed ETFs provide a lot of assets, but not as much in profits as actively managed funds. The actively managed funds that Blackrock manages tend to be a portion of the assets, but account for almost half of profits. Actively managed products accounts for a quarter of assets and half of revenues. Passively managed assets account for over 2/3rds of AUM, but half of revenues.

Blackrock has managed to grow organically, through new product introductions and through acquisitions. Given it massive scale, it is quite possible that new acquisitions will not have as big of an impact in the long-run. The massive scale does create advantages, since it spreads costs over a larger base, thus ensuring higher profits than smaller competitors. This also offers advantages in distribution as well.

Most asset managers manage to grow the bottom line by attracting new funds from new or existing investors, net of any that sell their holdings. Blackrock has done a great job growing assets organically and through acquisitions over the past decade. If financial markets rise over the next decade, it will also benefit from growing assets under management brought by higher prices. This is a two-edged sword however, because it leaves them exposed in the short-run by market volatility. I do believe that in the long-run, assets will likely go up, bringing a nice tailwind to investment managers such as Blackrock. If we get lower prices in the short run however, we will witness lower earnings per share and lower multiples. This is why I am buying those assets managers on the scale down.

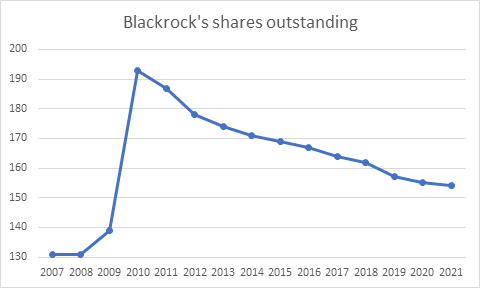

The number of outstanding shares increased between 2009 and 2010, due to acquisitions. That was the acquisition of Barclays Global Investors (BGI), which brought the iShares ETF franchise to Blackrock. Blackrock has been steadily reducing the number of share outstanding since then. Regular share buybacks can increase investors ownership interest in an enterprise, and automatically lift earnings per share. Companies have to be careful however not to overpay for shares they are retiring, otherwise they are wasting shareholder assets.

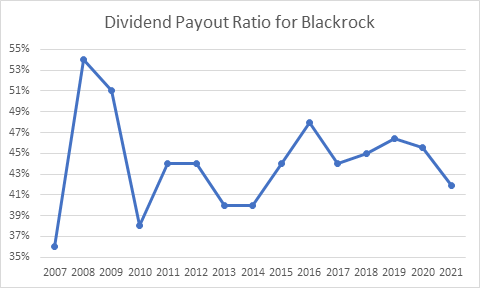

The dividend payout ratio has remained around 45% during the current decade; the only volatility occurred during the 2007 – 2009 financial crisis, when declines in assets under management resulted in lower earnings per share. The company did keep the dividend unchanged in 2009.

Currently, shares of Blackrock are valued at 22.33 times earnings and spot a dividend yield of 1.90%.

Relevant Articles:

– How to value dividend stocks

– Franklin Resources (BEN) Dividend Stock Analysis

– Eaton Vance (EV) Dividend Stock Analysis

– The Pareto Principle In Dividend Investing

Published at Sun, 16 Jan 2022 10:15:20 -0800