A. O. Smith Corporation (AOS) manufactures and markets residential and commercial gas and electric water heaters, boilers, and water treatment products in North America, China, Europe, and India. The company is a dividend aristocrat with a 28-year history of annual dividend increases.

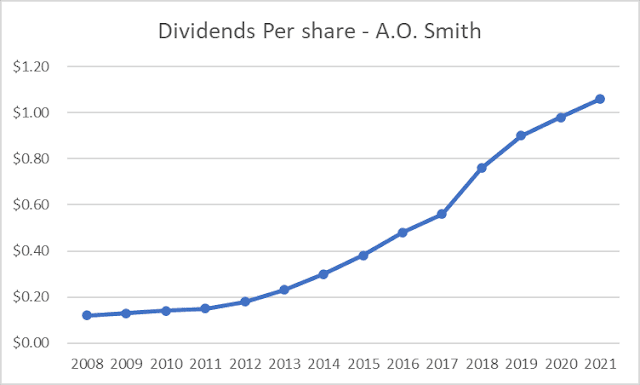

The last dividend increase occurred in early October 2021, when the board of directors approved a 7.70% hike in the quarterly dividend to 26 cents/share.

Over the past decade, this dividend aristocrat has managed to grow distributions at an annual rate of 21.50%/year. I expect reasonably high dividend growth over time, which may even exceed earnings per share growth for the next decade.

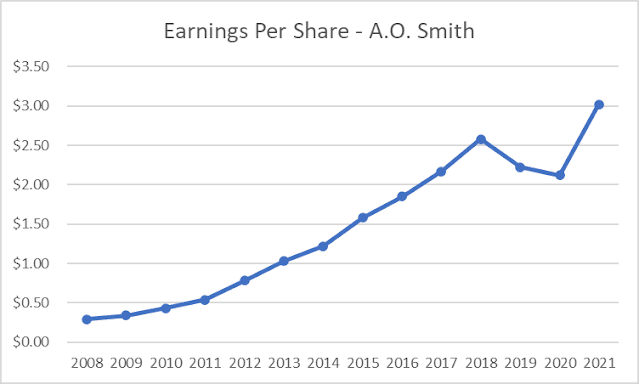

Adjusted earnings per share have experienced a steep uphill climb over the past decade, rising from 54 cents/share in 2011 to $3.02/share in 2021. The company is expected to earn $3.55/share in 2022.

A.O. Smith is a manufacturer of residential and commercial water heaters, boilers and water treatment products. It operates in two segments – North America with about two-thirds of revenues and Rest of the world with about a third of revenues.

Growth in earnings per share can be generated from rising demand from new construction for boilers and water heaters, as well as from need for replacements. The need for replacements of water heaters and boilers. A rising market share in China, along with growth in the Chinese market can bolster sales. International operations in general are expected to generate higher growth over time. The company can generate growth through new product introductions and through expanding of existing product lines. For example, the need for energy efficient units can drive sales down the road.

Strategic acquisitions can further boost revenues and earnings. Recent acquisitions allows A.O. Smith to enter the water treatment products market in North America.

A slowdown in China can lead to declines in revenues. A decline in housing starts could also negatively affect companies like A.O. Smith.

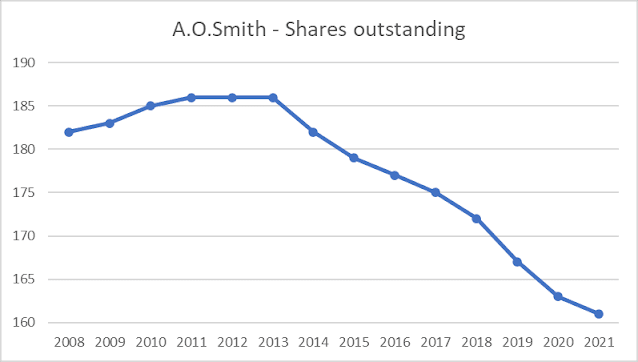

The company has reduced the number of shares outstanding by a little bit over the past decade, taking them from 186 million in 2011 to 161 million in 2021.

The dividend payout ratio increased from 28% in 2011 to 35% in 2021. Based on the expected earnings, the forward dividend payout ratio comes out to 32%. The company’s dividend is very safe and will likely grow at a higher rate than earnings over the past decade due to low payout ratio.

Currently, the stock is attractively valued at 17.17 times forward earnings at yields 1.85%.