Stock Market This Week – 03/18/23

Stock Market This Week

Stock Market This Week – 03/18/23

Stocks continued their trend downward. Contagion fears about the banking sector continue to keep investors on the sidelines. But the U.S. Government and Federal Reserve have moved decisively to contain the collapse of Silicon Valley Bank and Signature Bank. There are still fears about the impact of Credit Suisse’s difficulties, but the Swiss government is supporting the bank now, until solution is found.

Banking Deregulation and Failures

This failure resulted from the 2018 deregulation raising the threshold for stricter review to $250 billion. One consequence is that more banks will see tighter oversight. Also, the rating agencies will likely review credit ratings. As a result, I expect banks with a more significant percentage of uninsured deposits to receive rating downgrades. Also, banks and financial institutions can fail quickly once confidence is lost by investors, traders, and counterparties. Other companies may struggle for years before declaring bankruptcy or being bought by private equity.

The subprime mortgage crisis introduced the “too big to fail” concept for banks. But the government is now bailing out much smaller banks and their depositors. That said, equity and bond investors will take large losses.

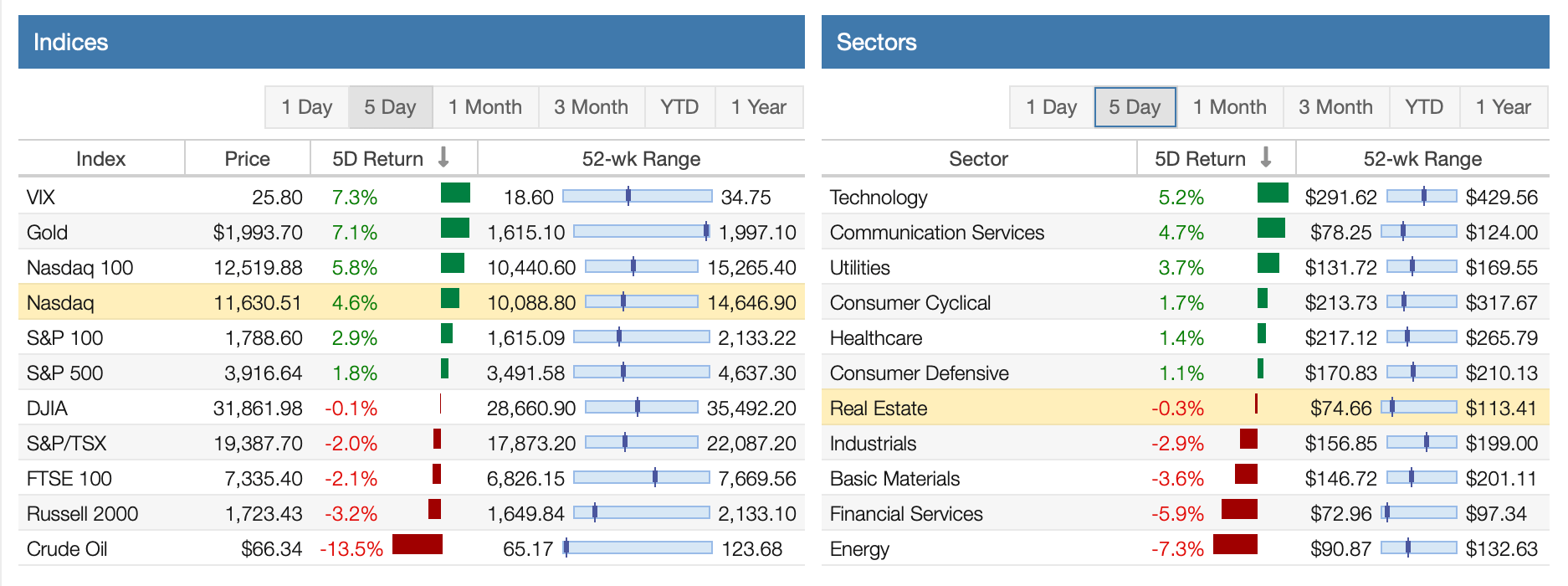

Stock Market Returns

As shown by data from Stock Rover*, the major indices had a mixed week. The Russell 2000 performed the worst because of the large number of banks in the index. The Dow Jones Industrial Average (DJIA) was flat. But the Nasdaq and the S&P 500 Index were up as investors moved into cash-rich tech and growth stocks.

In addition, oil fell significantly to its lowest price since 2021 on fears of weaker demand. But the VIX spiked by more than 7%.

Despite the awful headline news, 6 of ll eleven sectors had positive returns for the week. The Technology, Communication Services, and Utilities sectors led the way. The worst-performing sector was Financial Services at (-7.3%) as investors continued to sell banks, brokerages, and other companies. The Energy sector also performed poorly on low oil prices.

The Nasdaq is performing the best for the year, followed by the S&P 500 Index. The Dow 30 and the Russell 2000 are trailing with negative returns. In addition, 3 of the 11 sectors are up year-to-date. The three best-performing sectors are Technology, Communication Services, and Consumer Cyclical. The worst-performing sectors are Energy, Financial Services, Healthcare, and Utilities.

The dividend growth investing strategy has struggled with negative returns as banks and energy stocks declined. The table below shows their performance by category. All categories are now in positive territory.

Affiliate

Sure Dividend analyzes 850+ income securities every quarter in the Sure Analysis Research Database using the same metrics that matter in order to find the best income securities for members.

This is real research, not a quick computer screen. And all of this analysis is what powers the Sure Dividend Pro Plan. The Dividend Pro Plan includes:

- The Sure Dividend Newsletter focuses on investing in high-quality dividend growth stocks with a focus on expected total returns. It is Sure Dividend’s flagship newsletter. It always publishes on the first Sunday of the month.

- The Sure Retirement Newsletter focuses on investing in high yielding stocks, REITs, and MLPs. All recommendations must have a dividend yield of at least 4%. It always publishes on the second Sunday of the month.

- The Sure Passive Income Newsletter focuses on investing in high-quality dividend growth stocks with a buy and hold forever approach. It always publishes on the third Sunday of the month.

Dividend Power readers can use my Sure Dividend coupon code DP100 for $100 off the Dividend Pro Plan, reducing your price from $499/year to just $399/year.

Click here to start your 7-day free trial with the discount applied.

Dividend Increases and Reinstatements

Search for a stock in the list of dividend increases and reinstatements. This list is updated weekly. In addition, you can search for your stocks by company name, ticker, and date.

Dividend Cuts and Suspensions List

The dividend cuts and suspensions list was most recently updated at the end of February 2023. As a result, the number of companies on the list has risen to 616. Thus, well over 10% of companies that pay dividends have cut or suspended them since the start of the COVID-19 pandemic. The list is updated monthly.

Six new additions indicate companies are starting to experience headwinds in February 2023.

Stock Market Valuation This Week

The S&P 500 Index trades at a price-to-earnings ratio of 20.94X, and the Schiller P/E Ratio is about 27.97X. These multiples are based on trailing twelve months (TTM) earnings.

The long-term means of these two ratios are approximately 16X and 17X, respectively.

The market is still overvalued despite the recent correction and a bear market and rebound. Earnings multiples of more than 30X are overvalued based on historical data.

Stock Market Volatility This Week – CBOE VIX

This past week, the CBOE VIX measuring volatility ended at 25.51. The long-term average is approximately 19 to 20. The CBOE VIX measures the stock market’s expectation of volatility based on S&P 500 Index options. It is commonly referred to as the fear index.

Economic News This Week

Provided by Stock Rover*.

Consumer Price Index

The U.S. Bureau of Labor Statistics reported the consumer price index increased (+0.4%) in February, a slight deceleration from the (+0.5%) in January, but well above the (+0.1%) in December and (+0.2%) in November. Over the last 12 months, the all-items index is up (+6.0%) before seasonal adjustment compared to (+6.4%) in January. This marks the eighth month of a cooling in the annual inflation rate since it peaked at 9.1% in June.

The index for shelter was the most significant contributor to the monthly all-items increase, accounting for nearly 70% of the monthly reading. The shelter index increased (+0.8%) in February. The indexes for food (+0.4%), recreation (+0.9%), household furnishings (+0.8%), airfares (+6.4%), motor vehicle insurance (+0.9%), apparel (+0.8%) and new vehicles (+0.2%) all saw increases. The energy index decreased (-0.6%) as both the natural gas (-8.0%) and fuel oil indexes (-7.9%) saw significant declines. The indexes for used cars and trucks (-2.8%) and medical care (-0.5%) also declined. Core CPI inflation rose (+0.5%) in February, slightly from (+0.4%) for the previous month. The annual rate of core CPI inflation is now at 5.5%, down slightly from 5.6% in January. The shelter index is up (+8.1%) year over year, accounting for over 60% of the total increase in Core CPI.

Retail and Food Sales

The Commerce Department reported advance U.S. retail and food services sales fell 0.4% to $697.9B in February. January’s reading was revised to (+3.2%) from a previously reported (+3.0%). Retail sales, adjusted for seasonal shifts but not inflation, were up (+5.4%) year over year. Total sales for December 2022 through February 2023 were up (+6.4%) year over year. Sales decreased across multiple categories – led by department stores (-4.0%), home furnishings (-2.5%), restaurants (-2.2%), auto dealers (-1.8%), and miscellaneous retailers (-1.8%). Gasoline station sales dropped (-0.6%), reflecting lower oil prices. Internet retailers (+1.6%), health and personal care (+0.9%), and grocery stores (+0.6%) all saw increases. Excluding autos and gasoline, sales were up (+1.0%) for the month. Excluding autos, sales increased (+0.9%). Core retail sales, a measurement that excludes spending on cars, gasoline, building materials, and food services, increased (+0.5%) in February. This follows January’s upwardly revised (+2.3%).

Housing Starts

The U.S. Census Bureau reported housing starts increased by 9.8% to a seasonally adjusted annual rate of 1.450M units in February, down (-18.4%) from a year ago. Single-family housing starts, which account for the largest share of homebuilding, increased (+1.1%) to a rate of 830K units, down (-31.6%) from a year ago. Starts of five units or more increased (+24.1%) to a rate of 608K units, up (+14.3%) from a year ago.

New residential building permits, a proxy for future construction, rose (+13.8%) to a seasonally adjusted rate of 1.524M units. New residential building permits are running (-17.9%) below their February 2022 level. Single-family permits were up (+7.6%) from January’s revised 722K, down (-35.5%) from a year ago. Multifamily permits increased (+24.3%) to 700K. Leading the increase in building permits was the West (+30%), followed by the South (+10.9%) and Midwest (+9.6%). Only the Northeast saw a decline (-2.8%).

Single-family housing completions at 1.37M were (+1.0%) above January’s revised reading, while multifamily completions were up (+44.6%) to 509K. The number of houses approved for construction but have yet to start was unchanged at 294K units, with the backlog for single-family housing dropping (-3.0%) to 130K. The inventory of single-family housing under construction fell (-1.7%) to a rate of 734K units.

Curated Weekend Reading From Around The Web

Portfolio Management and Investing

Retirement

Financial Independence

Here are my recommendations:

Affiliates

- Simply Investing Report & Analysis Platform or the Course can teach you how to invest in stocks. Try it free for 14 days.

- Sure Dividend Pro Plan is an excellent resource for DIY dividend growth investors and retirees. Try it free for 7 days.

- Stock Rover is the leading investment research platform with all the fundamental metrics, screens, and analysis tools you need. Try it free for 14 days.

- Portfolio Insight is the newest and most complete portfolio management tool with built-in stock screeners. Try it free for 14 days.

Receive a free e-book, “5 Fundamental Metric to Check for a Dividend Growth Stock!” Join thousands of other readers !

*This post contains affiliate links meaning that I earn a commission for any purchases that you make at the Affiliates website through these links. This will not incur additional costs for you. Please read my disclosure for more information.

Prakash Kolli is the founder of the Dividend Power site. He is a self-taught investor, analyst, and writer on dividend growth stocks and financial independence. His writings can be found on Seeking Alpha, InvestorPlace, Business Insider, Nasdaq, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial sites. In addition, he is part of the Portfolio Insight and Sure Dividend teams. He was recently in the top 1.0% and 100 (73 out of over 13,450) financial bloggers, as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.

Published at Sat, 18 Mar 2023 07:38:09 -0700