Retirement Weekly: That get-rich-quick trade you’re missing out on

Relax.

By living your life and not bothering with the market’s and your portfolio’s daily gyrations, you’re not missing out on any strike-it-rich trade that would dramatically improve your retirement standard of living. In fact, according to a recent study from my performance auditing firm, you might instead be saving yourself from huge losses.

This week’s column is a continuation of last week’s theme, in which I countered the fear of missing out, or FOMO, that many retirees feel about alternative investments such as hedge funds, private equity, and so forth. This new study shows that we should also counter FOMO when it comes to the frequent trading of non-alternative investments such as stocks and bonds.

Any time is a good occasion in which to remind you that overtrading can be hazardous to your wealth. But it’s especially important in a bear market, such as this year’s, since many who otherwise recognize that frequent trading is a bad idea nevertheless believe that an exception should be made when the market’s major trend is down.

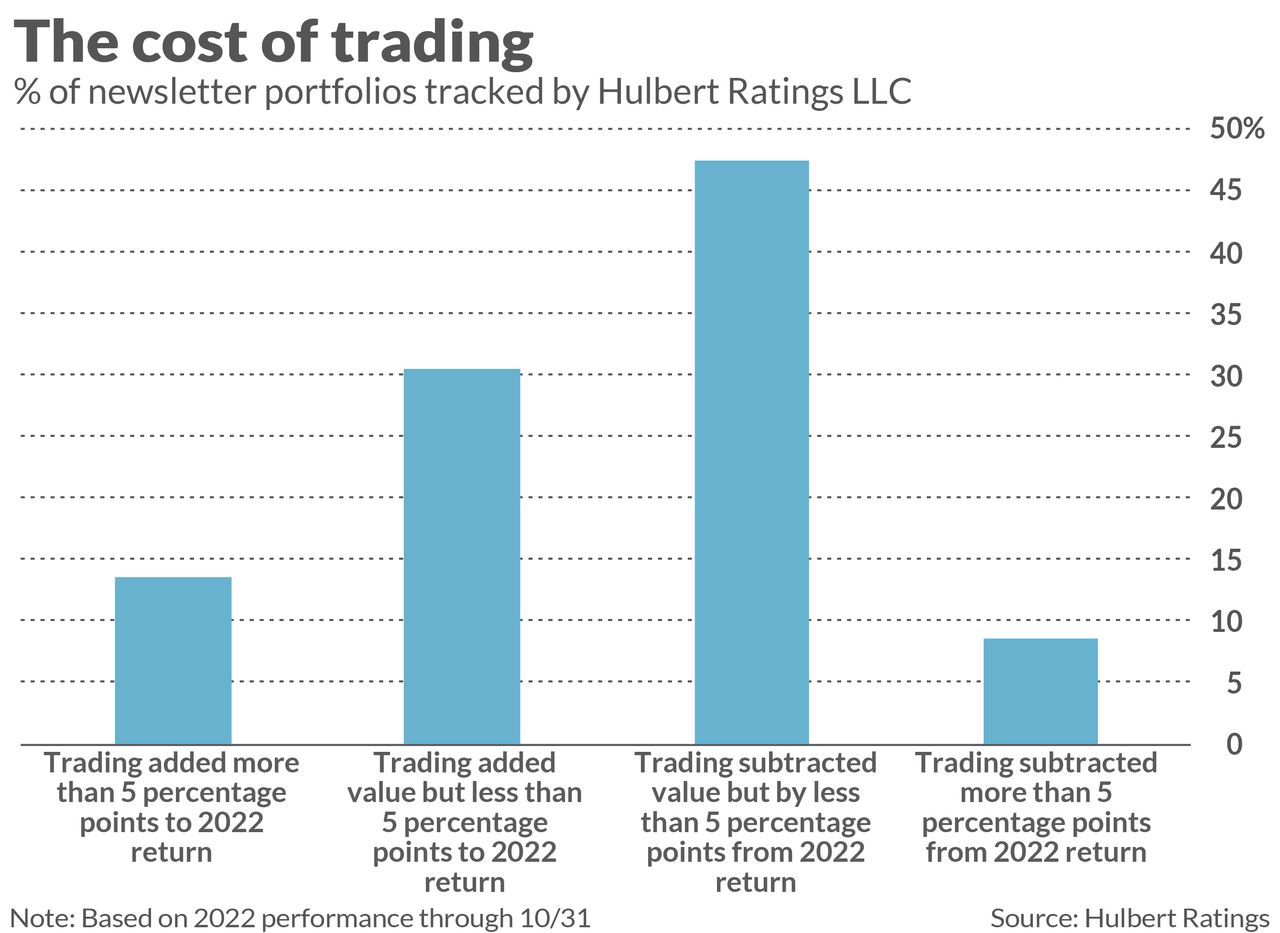

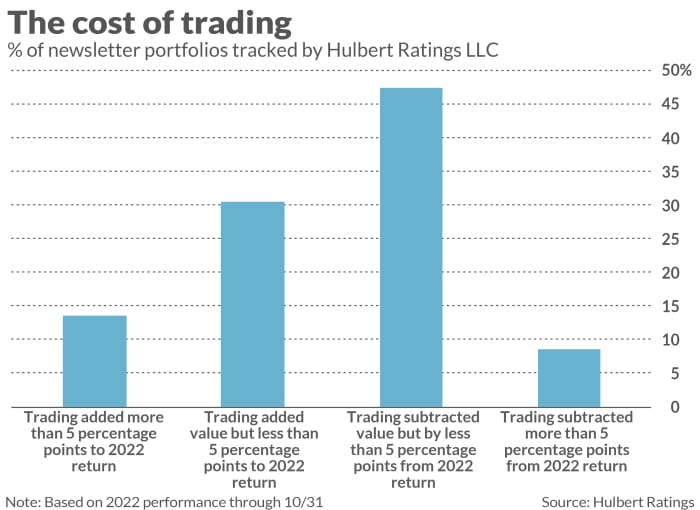

This study challenges that belief. The study calculated, for each newsletter portfolio that my auditing firm monitors, whether it today is ahead or behind where it would have been had it been frozen into place at the beginning of the year. Only if the actual portfolio is ahead of its frozen twin can we conclude that its trading added value.

On average this was not the case, as you can see from the accompanying chart. More than half the portfolios are behind where they would have been had they simply stuck with what they owned on Jan. 1. Across all monitored portfolios, actual returns on average were 57 basis points were worse than for the frozen portfolios—minus 14.2% versus minus 13.6% (through Oct. 31).

Note carefully that these statistics aren’t necessarily a criticism of newsletters. One way of interpreting the results is that it was because their advice at the beginning of this year was so good that it was hard to improve on it. Support for this comes from the above-market performance of the average frozen portfolio: Through Oct. 31, the Vanguard Total Stock Market ETF

VTI,

lost 18.7%, versus a 13.6% loss for the average frozen portfolio.

This year’s experience is not an exception, furthermore. My firm has conducted a similar analysis at the end of each year for more than two decades, and more often than not the actual portfolios lagged behind their hypothetical frozen twins.

Lest you think that these results are a unique feature of the investment newsletter industry, consider an identical study conducted three decades ago of the mutual-fund industry. It’s called “The Structure and Performance of the Money Management Industry,” the study’s authors were Josef Lakonishok of LSV Asset Management, Andrei Shleifer of Harvard, and Robert Vishny of the University of Chicago. Focusing on 12-month periods from 1983 through 1990, they found that the average actively managed mutual fund underperformed its hypothetical frozen twin by 0.78 percentage points per year. This is the same order of magnitude as the 57 basis point difference my firm found with investment newsletters so far this year.

Should you ever trade?

What if you nevertheless like trading? What if you enjoy focusing on the markets and your portfolio on a daily basis? Do the results reported here mean you shouldn’t?

Not necessarily. But you should take care to structure your portfolio so that your retirement standard of living isn’t impacted if your trading leads to a reduction in your return—as is likely.

One approach that makes sense was proposed decades ago by the late Harry Browne, editor of a newsletter called Harry Browne’s Special Reports: Divide your investible assets into two portfolios—one permanent and speculative. The former, which would contain the bulk of your assets, would be a buy-and-hold portfolio that you would rarely, if ever, trade. The second portfolio would contain your play money in which you could trade to your heart’s content.

Browne’s dual-portfolio approach is psychologically realistic in recognizing that many of us want to play the markets and trade frequently. But his approach is also financially and statistically realistic in recognizing that our trading is unlikely to add value over the long term.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com.

Published at Sat, 03 Dec 2022 09:46:00 -0800