Johnson & Johnson (JNJ), together with its subsidiaries, is engaged in the research and development, manufacture, and sale of various products in the health care field worldwide. The company operates in three segments: Consumer, Pharmaceutical, and Medical Devices & Diagnostics. This dividend king has paid dividends since 1944 and has managed to increase them for 61 years in a row. Dividend increases have been like clockwork every year for decades.

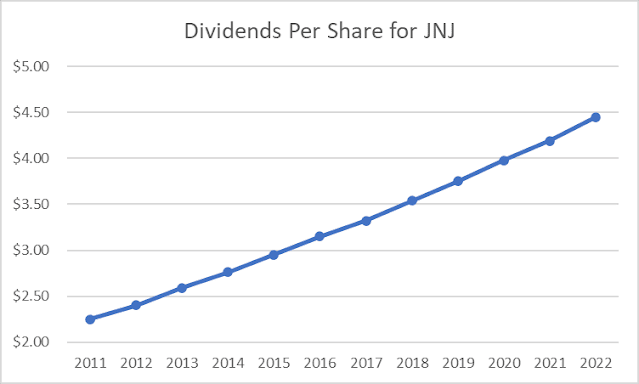

The company just raised dividends by 5.30% to $1.19/share. This is the 61st year of consecutive annual dividend increase for this dividend king.

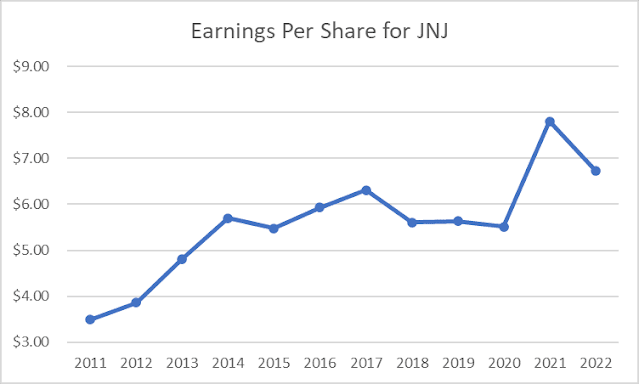

Johnson & Johnson earned $3.86/share in 2012 and managed to grow earnings to $6.73/share in 2022. The company expected to earn $10.51/share in 2023.

Johnson & Johnson has a diversified product line across medical devices, consumer products and drugs, which should serve it well in the future. This makes the company somewhat immune from economic cycles. Investors looking for a safe and dependable earnings can look no further than Johnson & Johnson. In addition, the company has strong competitive advantages due to its scale, leadership role in various diverse healthcare segments, breadth of product offerings in its global distribution channels, continued investment in R&D, high switching costs to users of its medical devices, as well as its stable financial position.

Future profits growth could come from new product offerings, which are the result of continued investment in research and development, and through strategic acquisitions.

Note that Johnson & Johnson announced a little over an year ago that it would likely be splitting into two companies – one focused on consumer products and the other on pharmaceuticals and medical technologies. It’s consumer health segment will be called Kenvue.

I am not sure how the dividend would be split yet. However, my guess would be that shareholders of legacy Johnson & Johnson would likely generate the same amount of total dividend income. It would just come from two companies, as opposed to one. I would give the spin-off some leniency in getting set-up. But if they do not pay a dividend within an year after the split, I may end up removing them from the portfolio.

Also note that Johnson & Johnson is involved in lawsuits related to its baby powder potentially causing cancer. The suits allege that this powder contains talc, which may have asbestos. These lawsuits could be costly in terms of damages to claimants, and loss of focus on management part. The company has tried to shield itself from those lawsuits by placing the affected subsidiaries in a separate company, and filing for chapter 11 for those subsidiaries only. This request has not been successful in shielding itself from this liability. This could potentially turn out to be very costly for JNJ. Or it could turn out to be a big nuisance, and the company could move on.

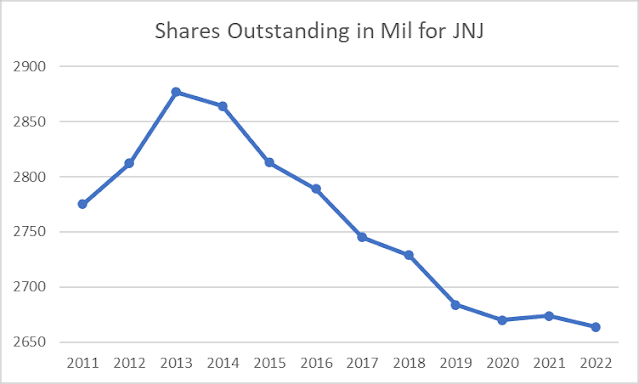

Johnson & Johnson has managed to reduce number of shares outstanding over the past decade, which helped earnings per share growth. Between 2011 and 2013, the number of shares went from 2,775 million to 2,877 million and then declined to 2,664 million. The short bumps up were related to acquisitions.

The company managed to grow its dividends by 6.40%/year over the past decade. The company’s latest dividend increase was announced in April 2022 when the Board of Directors approved a 6.60% increase in the quarterly dividend to $1.13/share.

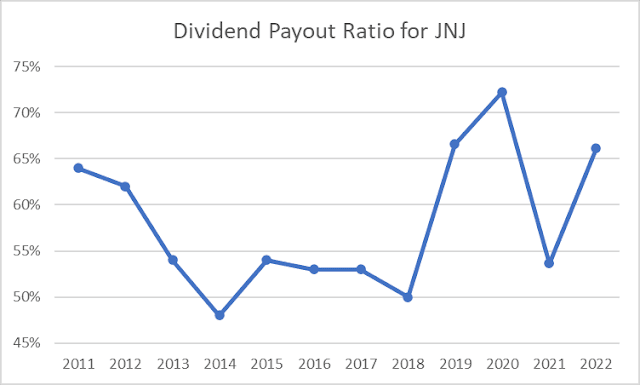

The dividend payout ratio has increased from 62% in 2012 to 64% in 2022. The ability to generate strong cash flows, have enabled Johnson & Johnson to reward shareholders with higher dividends for 60 consecutive years. I believe that the dividend is safe today, but will likely be limited to future growth in earnings per share of 5% – 6%/year over the next decade. A lower payout is always a plus, since it leaves room for consistent dividend growth and minimize the impact of short-term fluctuations in earnings.

Currently, the stock is fairly valued at 15.30 times forward earnings, yields 2.75% and has a forward dividend payout ratio of 40%.