Bristol-Myers Squibb (BMY) Dividend Stock Analysis

Bristol-Myers Squibb Company (BMY) discovers, develops, licenses, manufactures, markets, distributes, and sells biopharmaceutical products worldwide. The company is a dividend achiever with a thirteen year track record of annual dividend increases.

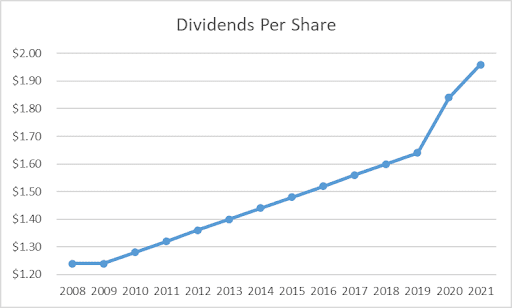

During the past decade, the company has managed to increase dividends at an annualized rate of 3.47%. The last dividend increase was in December 2021, when the company increased its quarterly dividend by 10.20% to 54 cents/share. I believe that future dividend growth will be higher than historical growth, due to the acquisition of Celgene.

Between 2010 and 2020, the company has managed to increase Non-GAAP earnings per share from $2.16 to $6.44. I use non-GAAP EPS because it is cleaner, and takes a look at a lot of one-time items or certain GAAP items that make looking at the business more complicated than it should be. Of course, the downside to this line of thinking is that management may decide to place regular and recurring expenses in the “special items” column, but refer to them as one-time.

Either way, the company is expected to grow Non-GAAP earnings per share to $7.35-$7.55/share by 2021.

Earnings per share will grow from finding new drugs, raising prices on existing ones, selling more, strategic acquisitions, and cutting costs.

In 2019, Bristol-Myers Squibb acquired Celgene for cash and stock. This diversified its drug portfolio, and provided an additional margin of safety against patent cliffs.

This deal was accretive to Bristol-Myers due to the fact that the P/E paid for Celgene was lower than the one that BMY stock had; In addition, the part that was financed through debt was accretive, because debt is very cheap today, and is well supported by the company’s strong cash flows. The company is also taking strides to repay it.

The company has six novel compounds in either early-stages of marketing or late-stages of R&D. These new drugs are mostly in the large market therapeutic areas of oncology and immunology.

While the company has a pipeline of drugs in different stages of approval, there is always the risk of regulatory delays and the risk that they fail to deliver what they were supposed to. Once a drug is approved, it offers its owners the right to be the exclusive seller for a 20-year period of time. This exclusivity comes to an end however, at which point branded drugs lose out market share to cheaper generic drugs.

It is also projected to generate cost savings or synergies. After all, the company gets to reduce headcount, decrease other expenses in the process, and generate incremental returns due to higher scale of operations. Of course, there is always integration risk, or the risk that the acquisition doesn’t turn out as expected, and the synergies that were expected do not get realized.

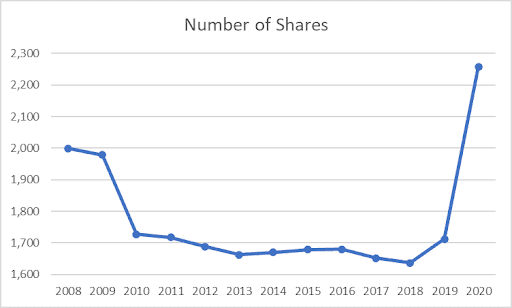

The number of shares outstanding decreased from 2 billion in 2008 to 1.637 billion by 2018. The acquisition of Celgene in 2019 has increased the number of shares outstanding to 1.712 billion in 2019 and increased it further to 2.258 billion in 2020.

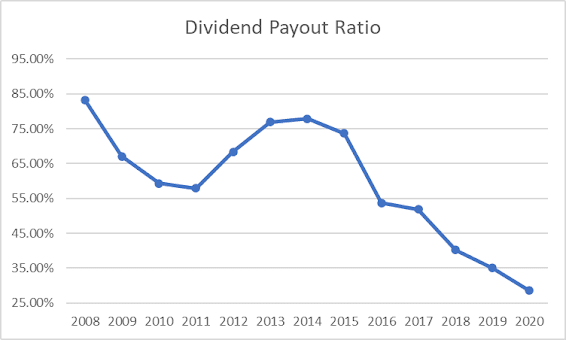

The payout ratio has decreased over the past decade, from 83% in 2008 to 28% in 2020. A lower payout ratio should provide a better margin of safety from short-term turbulence in earnings per share. It can also provide additional fuel behind future dividend increases. This can result in dividend growth that is faster than earnings growth for a period of time.

I find the stock to be attractively valued at 8.30 times forward earnings and a dividend yield of 3.47%.

Relevant Articles:

Published at Fri, 07 Jan 2022 05:31:51 -0800