Nephilim: Sons Of The 3x Bulls

DNY59/E+ via Getty Images

The Legend

The Nephilim were on the earth in those days, and also afterward, when the sons of God came in to the daughters of men, and they bore children to them. Those were the mighty men who were of old, men of renown.

Genesis 6:4

The Big Money In Leveraged 3x ETFs was published in May, 2020. Most of my development work since then has been feeble attempts to design effective ways of analyzing these instruments.

One tentative conclusion I’ve come to is 3x Bulls on Major Stock Indexes offer the simplest and best practical chance for an individual to quickly amass great wealth. The long-term numbers are so strong, that they should arguably be a standard component in larger portfolios.

My analytical methodology is driven by principles of applied information theory which I picked up in the school of hard knocks. New Concepts in Computational Finance describes some of the major design considerations, noting that they are quite similar to aspects of the work of Stephen Wolfram.

This methodology provides better market insights than a mathematical statistically oriented approach. The latest term to describe my techniques is Applied Information Theory.

Nephilim Logic

ETFs on major indexes were a major step forward in many different ways. For example, they allow longer analytical lookbacks without survivor bias, at some cost in granularity. 3x Bulls provide similar analytical benefits because of the artificially increased volatility.

Nephilim are created by holding a 3x Bull during the CO (Close to Open) finite state and holding a non-leveraged ETF during OC (Open to Close). The combined return streams create a new security.

Nephilim seems an appropriate term for the concept. At the same time, it is not easy to find a memorable term to describe non-leveraged ETFs, so here I use Daughters of Men to maintain the symbolism.

Creation Process

I modified my data build procedure recently to improve processing speed, and facilitate Nephilim logic. The performance part of the project went on for several months and got a bit intense. In all the excitement, I temporarily forgot about the Nephilim part.

The creation process is simple to explain:

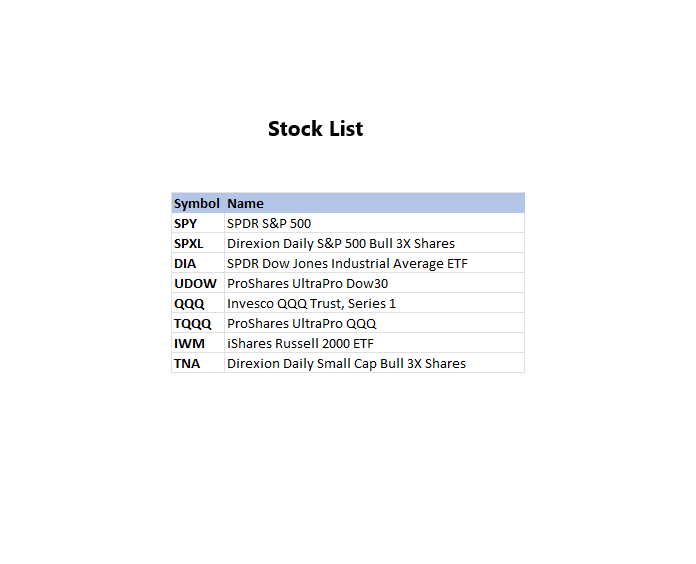

The Stock List

Stock List (JIFriedman.com)

The list is a worksheet that tells the algorithm what stocks to load for analysis, and the sequence they should appear in.

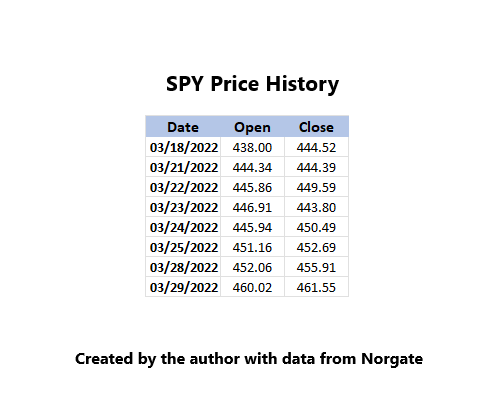

Stock Price History

SPY Price History (JIFriedman.com)

For each stock on the stock list, there is a txt file in a directory with price history for that stock that gets updated shortly after the market closes. The prices are adjusted for dividends and splits, etc. Norgate solves the technical issues of getting clean price history data.

The Build

Theoretically, one can go from the stock list and price history directly to produce any of my studies without creating any intermediate spreadsheets. That is a gradual process of course. As a practical matter, the open and close prices are not necessary after calculating daily natural log returns for the two finite states:

- CO – Close to Open

- OC – Open to Close

CC (Close to Close, or buy and hold) is also calculated, but that is a step that is not strictly necessary because with natural logs:

CC = CO + OC

It is useful to pre-calculate the natural logs for each symbol and store the results in a single worksheet to get access to information without doing multiple txt file opens and closes downstream which are slow.

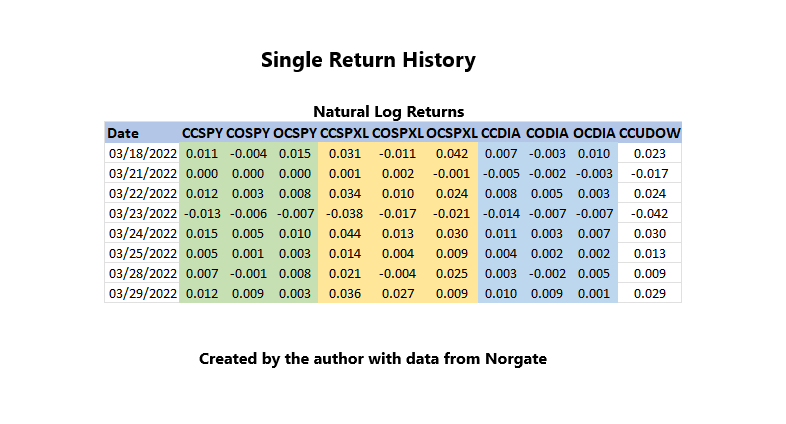

Single Return History Sheet (JIFriedman.com)

The Single Return History spreadsheet is laid out to allow very efficient and fast study building algorithms. The study building algorithms immediately convert the single return history spreadsheet into a two dimensional array (row, column). Address resolution between the return history input and study output is the technical challenge. Like I’ve said before, it takes a little practice.

With 16K maximum columns, Excel can handle over 5,000 individual stocks’ price history (3 columns per stock). Excel has processing constraints due to the need to meet normal customer requirements and at some point it can become an unsuitable platform. The issues got weird enough to modify my search patterns on YouTube and a Wolfram video popped up at some point.

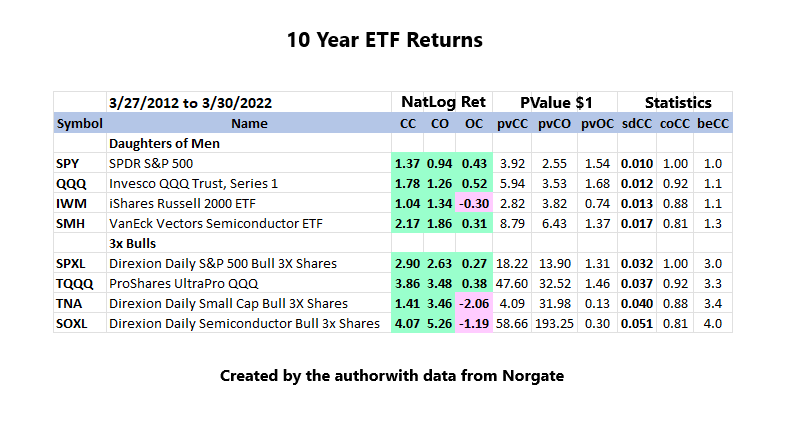

10 Year Performance

ETF 10 Year Performance (JIFriedman.com)

Buy and Hold performance for the period is in CC NatLog Ret, and shown in a more human-friendly manner in pvCC or present value of $1 invested at the period start.

The numbers are obviously overwhelmingly favorable for the 3x Bulls.

An investor is happy if a 3x Bull outperforms a non-leveraged instrument by a factor of 3 or more based on the present value of $1 invested in both at the start of an analytical period. That is a par amount.

More or less exactly the opposite will happen in a down market. In a down market, or intermediate downtrend, the investor will be lucky to not lose more than 3 times the non-leveraged instrument’s loss.

Statistics for the period include:

- sdCC – Standard deviation of the daily natural log return

- coCC – Correlation of the stock with SPY over the period.

- beCC – Beta of the stock versus SPY over the period.

The extra risk for the 3x Bulls is hinted at in the standard deviation. Most people can’t deal with the risk of…

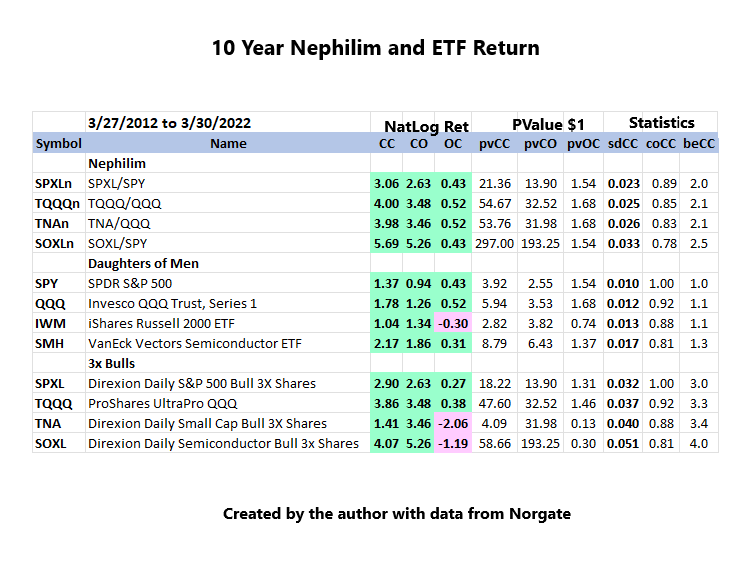

Nephilim Pairs and Performance

Nephilim and ETF 10 Year Performance (JIFriedman.com)

The Nephilim are given the CO mojo of the 3x Bulls and the relative OC serenity of the daughters of men. This makes Nephilim CC performance even more spectacular than the 3x Bulls. At the same time, volatility (or risk) is substantially reduced. SOXLn, for example, has virtually the same standard deviation as SPXL, but performance quality is also vastly improved because it now has a lower beta and correlation than SOXL has with SPY.

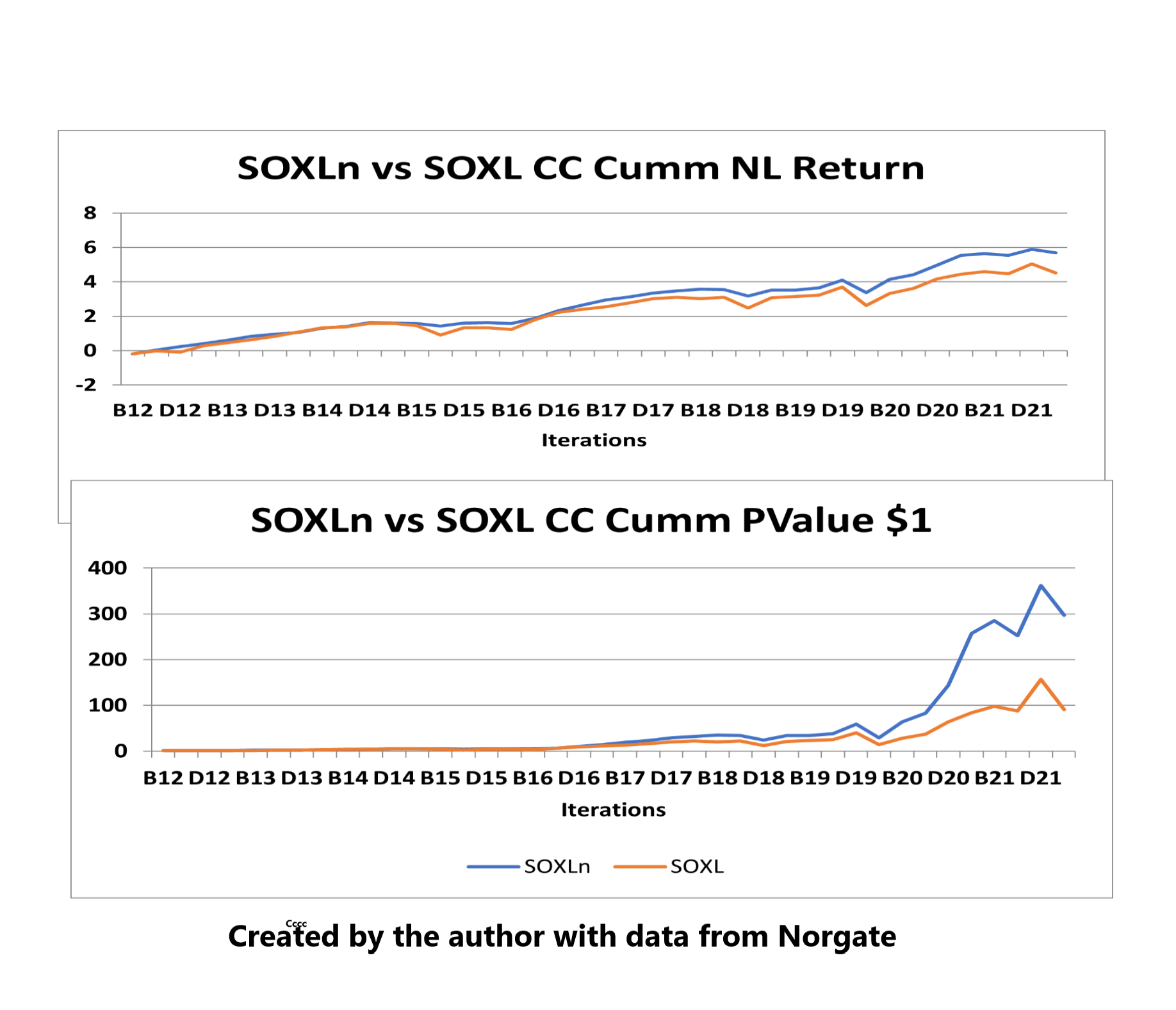

SOXLn versus SOXL Performance Through Time

The 10-year period can be broken into 40 periods (or iterations) of 63 days (or 3 months). Since there are 4 such periods in a year, each quarter is identified by an alpha code along with the year, so B12 corresponds to the second quarter of 2012.

SOXLn/SOXL Historical Performance (JIFriedman.com)

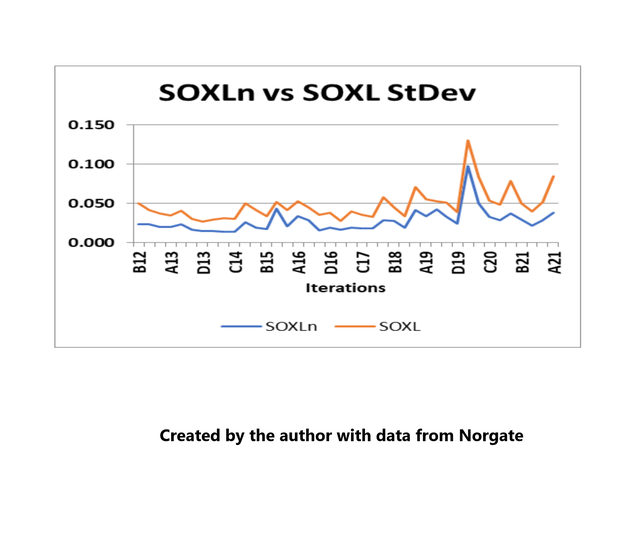

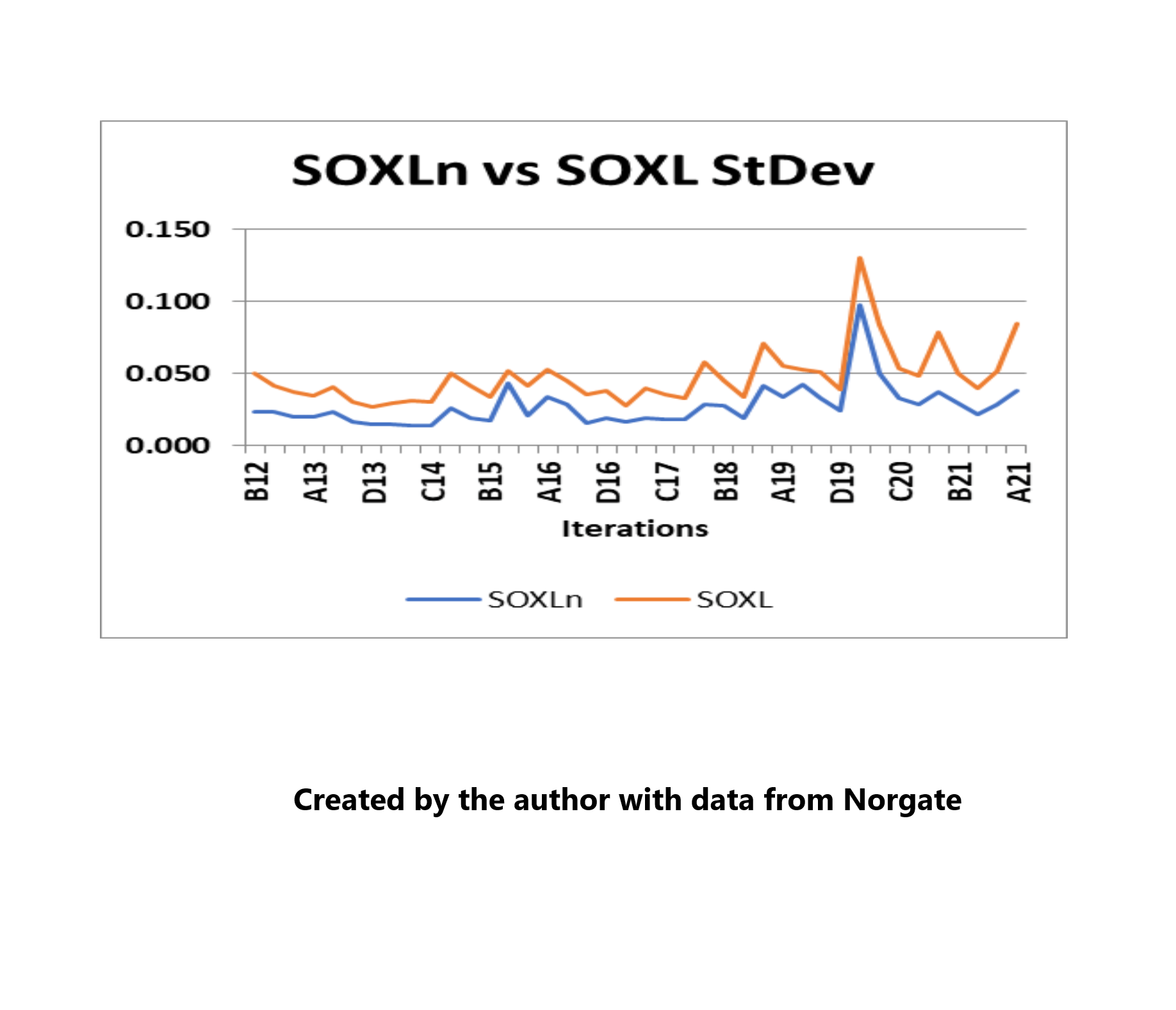

SOXLn vs SOXL Volatility (JIFriedman.com)

The StDev study shows that SOXLn is substantially less risky than SOXL, while the returns for SOXLn are far better.

It is possible to see the standard deviation of SOXL gradually increasing over the last 10 years. That is consistent with major indexes. It probably isn’t worth freaking out over.

Investment Methodology

It is important to understand how buy and hold works before an investor gets into trading tactics. Current action has shown the market to be in an intermediate downtrend that is close to ending because the current bounce looks stronger than minor.

If an investor missed the start of the collapse in early January, it was better to ride things out. Too much delta can turn a little turbulence into a personal catastrophe.

Published at Fri, 01 Apr 2022 21:34:29 -0700